Which analysts add value?

Analysts (and strategists and economists) are trying to bring order into the chaos of financial markets. But not all analysts are truly adding value. Some of them just reinforce the existing consensus, while others are shifting the consensus in such a way that the consensus view is getting better and more accurate than without that input, which brings us to the question of whether analysts really add value and, if so, who does and who doesn’t.

A commonly held belief among many investors is that sell-side analysts don’t add value and that their recommendations and insights do not create outperformance. But as I have previously discussed, this seems to be the case in the US stock market, but not elsewhere.

One of the problems that every investor has is which analyst to trust when it comes to specific stocks or markets. Plus, if this analyst disagrees with the consensus, how much weight should you give to the analyst vs the consensus?

Naman Kumar from Carnegie Mellon University developed an interesting approach to tackle these questions. He was inspired by the Shapley Value used in machine learning and other applications. In essence, the Shapley Value measures how much a specific input improves the accuracy of the output. In machine learning, the job is to remove input variables with low Shapley Value to get to a halfway tractable model.

And in a way, the job is similar for investors. They must figure out which analysts are adding value and which ones can be cut out of the consensus or the inputs to the investment process of managing a portfolio.

Of course, this is in practice mostly a qualitative assessment (though many hedge funds run alpha capture models that do this quantitatively), but his research gives us some pointers on where to look for good analysts.

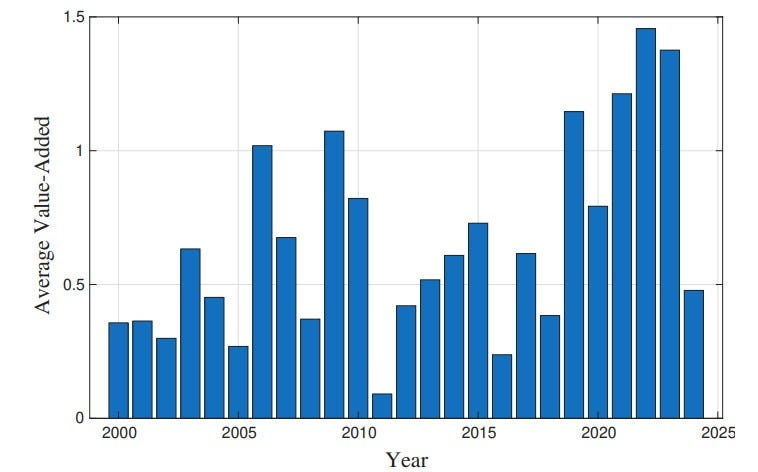

First, the good news is that the average value-added of equity analysts tends to increase over time and is particularly high during times of market turmoil like the 2008/09 financial crisis, the pandemic of 2020 and the inflation spike in the aftermath of the pandemic of 2022/23.

Average analyst value-added

Source: Kumar (2026).

That’s good news for people like me and my colleagues who are trying to keep our jobs in a market that is increasingly dominated by passive investors. On average, we are not useless, it seems.

But among us analysts, what kind of characteristics should you look for? Here are the key results (and remember, they apply on average, not to any specific individual):

Analysts who deviate more from consensus tend to be more informative and tend to improve the accuracy of markets.

More experienced analysts tend to be more informative, which is why the juniorisation that happened in large investment banks over the last two decades probably has decreased the value of their research.

Indeed, all-star analysts and analysts at large brokerage firms tend to add less value than analysts at smaller firms (which I wholeheartedly agree with; until, of course, I get a call from Goldman Sachs to hire me as their new European equity strategist…).

Analysts who update their forecasts and views very quickly after an earnings release or very late after an earnings release tend to be the ones who add the most value. The former because they are responsive and can shape investor reaction to news, the latter because they typically offer deeper insights that require some digging to get to. The analysts that are in the middle of the pack in terms of timing their recommendations are the ones that typically add little value.

Forecast accuracy, interestingly, does not correlate with value-added. There are analysts with very accurate earnings forecasts that add little value to investors and some that add a lot. Similarly, if an analyst has huge forecast errors, it might not lead to low value added for price discovery and investors’ decisions.

Overall, what you should be looking for is an experienced analyst who works for a smaller firm and isn’t afraid to make contrarian calls based on well-developed analysis. And this person ideally should be very reactive when markets are in turmoil or take time to come to a conclusion. Ideally, this person should do both, provide guidance in the middle of a chaotic market, but also deliver well-considered arguments once the market has calmed down again.

The accuracy finding is the one that matters here, and the Shapley framing is exactly why. Value-added measures marginal contribution to the consensus, which is a different quantity from being right about the number. An analyst can nail the EPS to the cent and add nothing, because that estimate was already in the price, and another can be wrong on the print and still add value by shifting the distribution toward where it belongs. Accuracy scores the forecast. Shapley scores the information.

Seen that way, the whole trait list collapses into one variable. Deviates from consensus, experienced, smaller firm, willing to be early or late and never mid-pack: each is a proxy for the same thing, an input the market does not already contain. Accuracy is missing from the list because correctness and non-redundancy are orthogonal. Being right and being worth listening to are different jobs. Only the second moves the price.