Why are analyst forecasts so optimistic: Growth assumptions

At the start of each year, I write about how useless forecasts by strategists and analysts are. One thing that is persistent in these forecasts is that fair value estimates by equity analysts tend to be overly optimistic while forecasts from strategists tend to be too pessimistic. But why are the target prices of analysts for stocks they cover on average too high?

An examination of 78,000 sell-side analyst reports allowed Paul Décaire and John Graham to find some common trends.

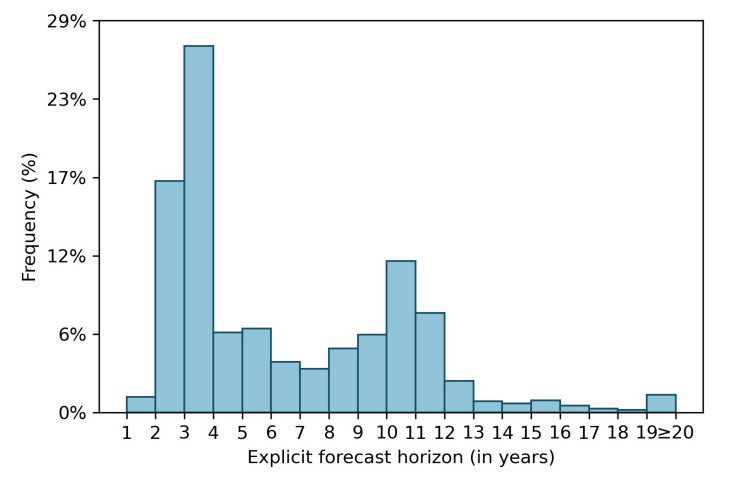

Every analyst knows that most of the fundamental value of a stock is hidden in the long-term outlook for future cash flows. Typically, an analyst will explicitly model free cash flow growth for the next three years or so and then assume that growth will revert to some terminal long-term average forever. I know, once you state it explicitly it makes you cringe at how nonsensical this approach is, but so be it.

Number of years explicitly modelled by analysts

Source: Décaire and Graham (2024)

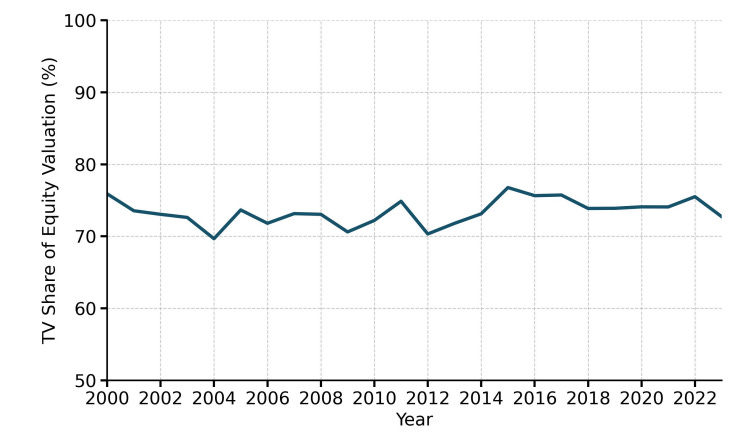

The result of this common practice is that the terminal value typically accounts for about 75% of the total fair value. And that share is remarkably stable, indicating that analysts really don’t change their approach to modelling over time.

Terminal value share of total fair value

Source: Décaire and Graham (2024)

But what kind of growth do analysts model for the immediate future and for the terminal value? Over time, the terminal growth rate has declined to something like 2.1% per year. That is pretty conservative and shouldn’t lead to overly optimistic equity valuations.

The true sin of analysts is how they model growth in the first three to five years in the future. The chart below is eye-opening in its ridiculousness. It shows the average growth rate assumed by analysts in the first three to five years ahead (the period they model explicitly) together with the terminal growth rate used to derive the value of all future cash flows after the explicitly modelled future.

Analyst growth assumptions for the next three to five years (red) and the years thereafter (blue)

Source: Décaire and Graham (2024)

Apparently, the stocks analysts cover manage to grow free cash flows by 12% to 16% per year for the next three to five years and then all of a sudden, growth drops down to about 2% per year.

Also, note how growth rates for the next three to five years vary systematically with the market environment. When markets are going up, the growth rates are adjusted upwards as analysts struggle to justify higher valuations of the stocks they cover.

Then markets crash like in 2001 and 2022 and analysts are loathe to revise their target prices downward. So they adjust their growth expectations even higher to justify their excessively optimistic target prices.

As the stock market recovers, an analyst can reduce their growth assumptions again because the actual share price moves closer to their target price. Of course, eventually, stock markets rise beyond many of these target prices and the entire cycle starts again.

This is why I always recommend investors take a close look at the growth rates analysts price into their models for the next three to five years. This is where they fudge their models to fit the present, and where they become overly optimistic to justify overvalued markets.

I was a sell side analyst for 16 years, and there are massive institutionalized psychological and job preservation reasons for what you've observed. You say "[t]his is why I always recommend investors take a close look at the growth rates analysts price into their models for the next three to five years. This is where they fudge their models to fit the present, and where they become overly optimistic to justify overvalued markets." I couldn't agree more, but even healthy scepticism shouldn't always drive one to simply haircut the assumptions ... sometimes they're actually way too conservative.

Walk into your morning meeting as an analyst and present a buy recommendation with a price target 50-60% higher, and your salespeople will tell you "that's ridiculous", my clients will laugh you out of the room". Cook up a target 5-10% higher, and they'll say "my clients won't even cross the street for that ... and if you really feel that way, then why isn't it a "hold" or a "sell"? I've never seen any academic work on it, but I'd bet the median street analyst target price upside is +20-30%, because that's the range everyone seems to feel is "reasonble" and/or "attractive", and not "ludicrous".

Even though 95% of all ratings are "buy" or "hold", and 60% of that 95% are "buys", no one ever seems to notice that having over half the market mis-priced to the tune of 25% doesn't exactly jibe with the efficient markets hypothesis. It's like Lake Wobegon, "where all the women are strong, all the men are good-looking, and all the children are above average" https://en.wikipedia.org/wiki/Lake_Wobegon . Also, on the banking prospect side of things, sitting with your firm's investment bankers at a company pitch and telling management that you're valuing their stock using a GDP-minus 2% terminal growth rate is definitely not career enhancing.

I think the bigger issue is that there are too many examples where slavish devotion to terminal value DCF modeling has kept people away from some seriously great 20-year stocks: Apple Computer stock has compounded up 30% per year (!) from $1.25 to $247 over two decades; modeling modest assumptions about growth reversions in mobile 'phones wouldn't have gotten you anywhere. Amazon.com stock went from $2.21 to $213, +26% per annum. Even the stock of Microsoft, now an almost half-century-old company, went from $26 to $398, +15% per annum over that 20-year timeframe. Now, with that perfect knowledge, climb into your time machine, go back to 2005, and write three research reports using 30%, 26%, or even a 15% terminal growth rate assumptions in your DCF modeling to produce +19,660%, +9,538%, and +1,431% price targets, respecively, and see how long until you'd've lost your job and been hauled off to the loony bin.

Then there are stocks that used to be called "concept stocks" that are all over the place, seemingly driven solely by animal spirits. A car company should be pretty simple to value, but Tesla stock was $250 last Halloween, $450 right before Christmas, and is back to $300 today. Palantir stock is down 30% in the past week, but even after that it's trading for 70x sales and 450x earnings. Any attempts to slap a DCF on those would clearly not assume reversion to a 2% growth rate.

In fact, the whole Magnificent Seven appears to be an "exception that proves the rule" exercise https://en.wikipedia.org/wiki/Exception_that_proves_the_rule ... let's just hope it's not another Nifty Fifty https://en.wikipedia.org/wiki/Nifty_Fifty .

survivorship bias speaking here:

most of my success in investing has been holding on to sensible american GARP fund managers. they have underperformed megacap indexes, but have been disciplined for exiting meme multiples which seems to have been a credible risk lowering tactic.

i do not discount the role of luck for them , as they still need a few % differentiated weight profile to win. remarkably, they have all lost money flows and re-opened to new investors. some managers have not embraced an active ETF structure.

as a few times in the past, i wonder if this is the end for active growth success.