Active managers get competition from AI

Active managers get competition from AI

One of the key advantages active managers have over index trackers is that they can analyse qualitative data and the context for company fundamental data. Analysis of data in its context and with the nuances given by a company in its annual reports and conference calls should in theory enable the skilled active manager to outperform an index. Obviously, the fact that most actively managed funds underperform their benchmarks after cost shows that not all fund managers are skilled or skilled enough to justify their fees. But alas, being able to evaluate qualitative information is a key advantage active managers have. Or should I say had?

Alex Kim and Valeri Nikolaev from the University of Chicago showed that AI can be used to assess this qualitative information and increase performance this way. In essence, they trained a natural language processing model to analyse the context for the profitability of a company provided in the Management Discussion & Analysis section of US company reports (you know, the stuff that allows you to identify fraud and future earnings disappointments).

Training the AI on financial reports released between 2019 and 2021, they then analysed the information published in 2022 to sort companies by operating profitability as reported or context-specific operating profitability where the AI adjusted operating profitability slightly up or down based on the qualitative information given by the management.

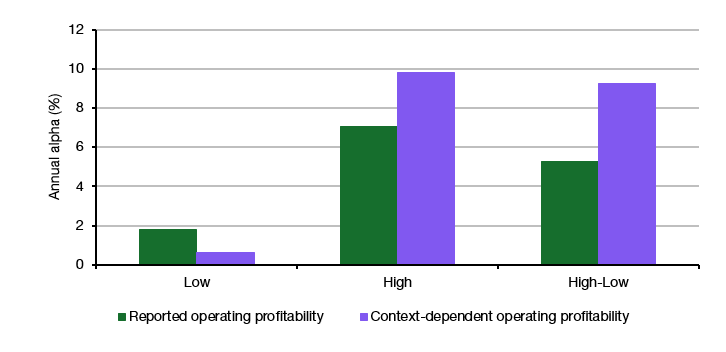

Below are the resulting differences in portfolio alpha when adjusted for the usual five factors of Fama and French (market risk, value, size, investment intensity, and profitability). Using qualitative information enables investors to better differentiate between highly profitable and less profitable companies, just like skilled active managers can. And that is why AI is such a double-edged sword. It provides additional competition to white collar jobs but at the same time can increase productivity for white collar workers who embrace the technology and incorporate it into their processes.

Alpha of companies with different levels of operating profitability

Source: Kim and Nikolaev (2024)

The most significant risk is to fresh graduates and people working in jobs where a good enough AI is needed and not a perfect one to replace a role or portion of the jobs. If the below is accurate, the first shot has already been fired, which means others will try, and a very few CEOs will not be willing to cut the cost to improve their stock price.

Last week, Sebastian Siemiatkowski, CEO of Klarna, gave some more details (https://www.exponentialview.co/p/the-ai-squeeze?utm_source=post-banner&utm_medium=web&utm_campaign=posts-open-in-app&publication_id=2252&post_id=145468103&triedRedirect=true):

Due to the implications of AI since September, October [2023], we have stopped recruitment, and in our case, with normal attrition rates that most tech companies have, where people stay about five years… this means that we are actually shrinking in number of employees by about 20% per year.

So we hope that by the time we kind of get to that perspective, we’re going to be able to present something that looks like revenue growth while costs actually diminishing at the same point.