The impact of future deficits on US Treasuries

The impact of future deficits on US Treasuries

I emphasise from time to time how the large amount of debt the US has is unlikely to lead to default. Most recently, I have discussed that thanks to the privilege of issuing the world’s reserve currency, the US can borrow much more than other countries without risking higher interest rates. But that doesn’t mean that higher indebtedness has no consequences. If the US borrows more, it has to pay a higher price for it.

A team of researchers around Hanno Lustig from Stanford examined the reaction of US Treasury markets to announcements by the Congressional Budget Office (CBO) on the fiscal impact of proposed legislation. By law, the CBO must ‘score’ all proposed legislation on a ten-year horizon and estimate its likely impact on government borrowing.

There are also some arcane rules about laws that must be fiscally neutral after ten years or they must be passed as part of the budget. This is why so many US spending laws have sunset provisions where tax cuts are reversed in year nine to make a bill fiscally neutral on that artificial time horizon. For example, the Trump tax cuts of 2017 reduced personal income tax rates for the highest earners and increased inheritance tax thresholds from $6m to $13m. At the start of 2026, these tax cuts will be reversed automatically unless Congress passes a new law to extend them. This was done to ensure that between 2017 and 2027, the Trump tax cuts were within the limits set by the CBO for fiscal spending.

Using more than 1,000 CBO assessments of Congressional legislation in the US between 1997 and 2022, the researchers found that Treasury markets show a significant reaction to uncovered deficit spending. They find that over this 25-year period about 57% of government spending was not covered by higher revenues (and before you complain, both parties are guilty as charged). And the uncovered debt spending leads to higher Treasury yields while increased spending that is covered by higher revenues does not.

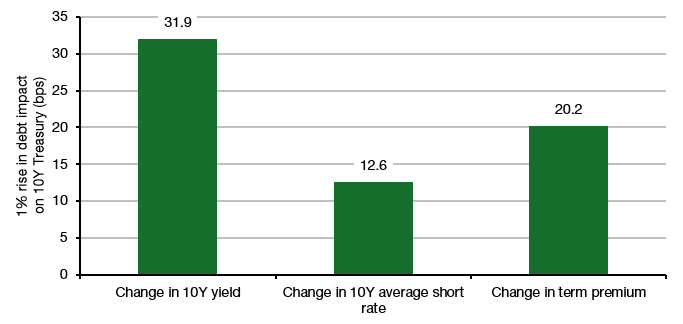

The researchers found that for every 1% of GDP increase in US debt, 10-year Treasury yields rise by c.32bps. This change is driven by market expectations for short-term interest rates over the next decade rising by 12.6bps and the term premium of 10-year Treasuries over short-term bonds rising by 20bps. In the end, every American pays for uncovered government spending in the form of higher mortgage rates, higher business loan costs, etc. If you are American (or British, or French, etc. where this arithmetic applies qualitatively as well), you might think about that the next time your government talks about cutting taxes or increased spending.

Impact of 1% increase in US indebtedness vs. GDP

Source: Gomez Cram et al. (2024)

'both parties are guilty as charged'. Yes. And i am no lover of dems since they seem so happy competing with reps on 'who has the most wackos?' (For generations, western European media followed a very simple scheme: America is bad when ruled by a rep, and good when ruled by a dem. I.e. 'people who sort of resemble us are okay'. It seems that qualifier is now applied not just to politics but to basically every subject).

But when it comes to deficits there is a difference (until Biden of course):

Reagan start $78.9 B def / End $152.6 B Increased def

Bush 41 start $152.6 B def / End $255 B Increased def

Clinton start $255 B def / End $128.2 B + Surplus

Bush 43 start $128.2 B + / End $1.41 T Increased def

Obama start $1.41 T def / End $584.6 B Decreased def

Trump start $584.6 B def / End (19’ pre covid): $1.1 T Increased def

Biden - never mind…

PS Are you enjoying US/European media's 'surprise' about Biden's debating 'skills' as much as i do? It seems that after lying to the public for years they have now turned on themselves: 'how were Biden's confidants able to mislead us?'

Guess how...

There are no free lunches

...but there are only limited short-run repercussions for excess government borrowning which are further reduced by being the source of the reserve currency.

I somehow don't think that I could have a career as an author of catch aphorisms :(