A macro forecast of stock and bond returns

One of the most important things I have learned in my career is not to listen to macroeconomists making forecasts of financial assets. They have no clue and their forecasts generally are so wide off the mark as to be useless.

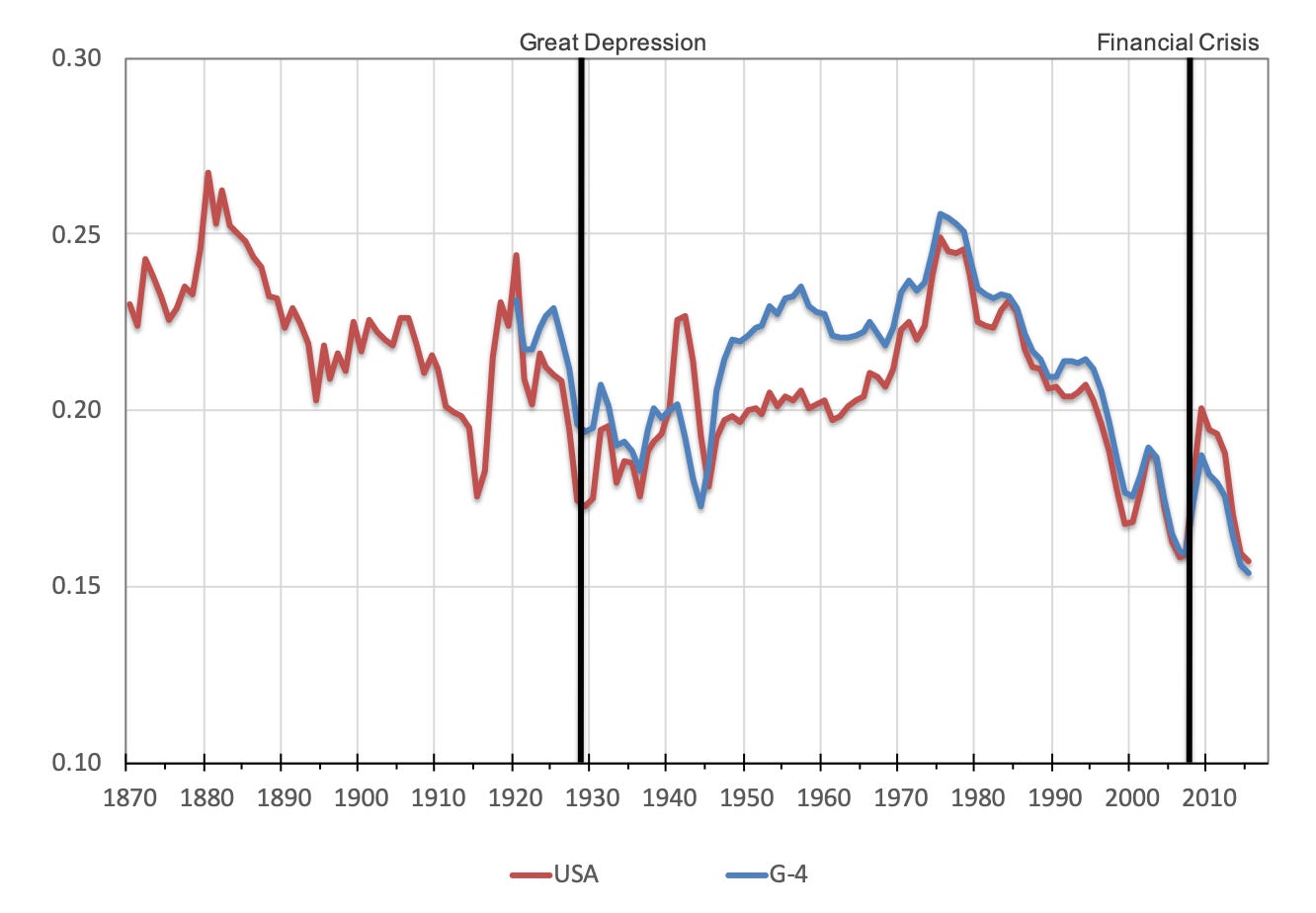

However, there are exceptions to the rule and one such exception is the link between consumption and future real interest rates. If you look at the ratio of private consumption to private wealth, you can see that it tends to decline slowly over time but has long-lasting secular swings. Periods of high consumption to wealth are followed by extended, often decades-long periods of low consumption to wealth. This makes intuitive sense because if consumption is high relative to wealth, then subsequently, consumption must slow down as households deleverage their balance sheets or the returns on wealth must increase to catch up with previous consumption. Higher returns on wealth are possible if either real rates are high (and thus returns on bonds are high) or risk premia on equities and other risky assets are high.

Unfortunately, in the aftermath of both the 1920s and the early 2000s we have seen a decline in consumption to wealth that is mostly driven by lower consumption after households got too leveraged (e.g. through excessive mortgages) and suffered a significant decline in wealth during the subsequent financial crises. Meanwhile return on wealth was very low during the crises and real rates turned out to be negative after the crises for some time.

Consumption to wealth ratio

Source: Gourinchas and Rey (2019). Note: G-4 = Average of the USA, UK, Germany, and France.

This is a problem because consumption to wealth is highly predictive of future real interest rates. If households consume less relative to their wealth, then global demand grows at a slower pace than in the past and investment returns drop. Furthermore, if households not only consume less but safe more to repair their highly leveraged balance sheets, then the resulting savings glut implies that too many savings are chasing too few investment opportunities and interest rates have to drop. In fact, a study by Pierre-Oliver Gourinchas and Helene Rey shows that the consumption to wealth ratio is highly predictive of real rates up to ten years into the future.

The chart below shows their predictions for the average real interest rate in the G-4 countries (USA, UK, Germany, and France) from 2015 to 2025. The chart not only shows that in the past, consumption to wealth ratios have been able to predict real rates quite well, it also shows that the real rates may stay negative well into the mid-2020s. The average real interest rate for the United States is predicted to be -2.35% and for the G-4 it is predicted to be -3.1%. In other words, we have to be prepared that we will not normalise interest rates for a very long time – something I have talked about here and here.

Predicted real rates in G-4 countries

Source: Gourinchas and Rey (2019). Note: G-4 = Average of the USA, UK, Germany, and France.

Another financial variable that can be predicted reasonably well with the consumption to wealth ratio is the term-premium of long-term bonds over short-term bonds. Historically, lower short-term rates implied a higher term premium for long-term bonds and thus, the prediction of lower real rates indicates that the term premium on long-term bonds relative to money market rates should increase in the ten years from 2015 to 2025 and reach around 2% on average.

Predicted term premium in G-4 countries

Source: Gourinchas and Rey (2019). Note: G-4 = Average of the USA, UK, Germany, and France.

However, just to show you that you can do much harm with macro forecasts of asset returns, the chart below shows the predictions for the equity risk premium over bonds in the years 2015 to 2025. The authors of the paper note explicitly that the consumption to wealth ratio has no predictive power for the equity risk premium and the chart shows that the difference between realised and predicted equity risk premium is all over the place. Nevertheless, that does not prevent some macroeconomists from using this and similar variables to make daring forecasts about declining equity returns.

Predicted equity risk premium in G-4 countries

Source: Gourinchas and Rey (2019). Note: G-4 = Average of the USA, UK, Germany, and France.