Blame big tech for the lack of IPOs

Here in the UK, there is an intense debate about the dearth of IPOs, but even in the US, more and more venture capital-backed companies choose to stay private for longer rather than IPO. And according to Florian Ederer and Bruno Pellegrino, there is a case to be made that the dominance of big tech companies contributed to this trend.

It is no surprise that we had hardly any IPOs in 2022. Inflation and interest rates were rising rapidly, and uncertainty was high. But even in 2023, the IPO market was slow to get off the starting blocks, though it is increasingly showing signs of life and IPOs are becoming more numerous. Nevertheless, the overall trend shown in the chart below is simple: More and more start-ups are choosing to sell themselves to larger competitors rather than go public.

IPOs and acquisitions of VC-backed start-ups in the US

Source: Pitchbook

What is driving this trend (at least partially) is the opportunity cost of going public, according to Ederer and Pellegrino. If a start-up decides to go public, it must compete with the big incumbents in its sector. That means it will face hurdles like technological compatibility, a smaller marketing budget, and other factors. In other words, the large incumbents can make life hard for you while your shareholders demand relatively rapid progress in growth.

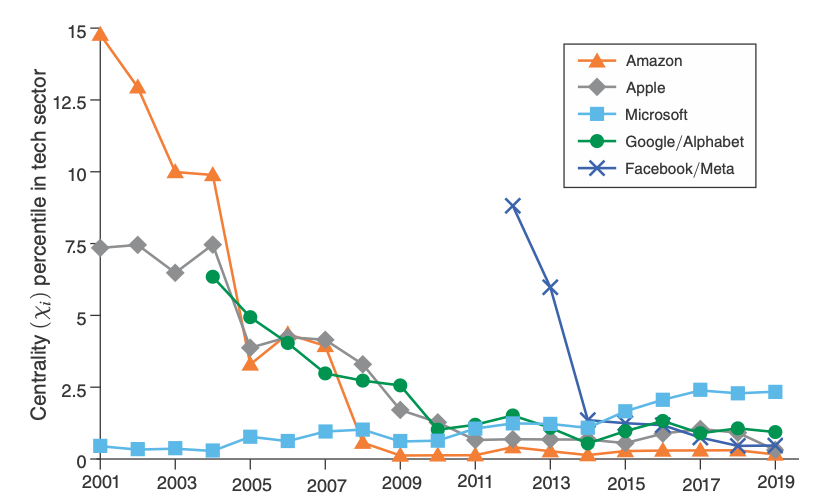

And the more entrenched a technology is, the easier it is for the silverback gorilla in a sector to make life harder for disruptors. Look at the chart below which shows the market centrality of the large US tech companies. The lower the score, the more central their products are for a given industry and the harder it is to dislodge them and convince customers to switch to competitors. While Microsoft has suffered a small drop in market centrality (its moat has slightly narrowed) the others have all seen their moat grow massively over the last 20 years.

Market centrality of big tech companies

Source: Ederer and Pellegrino (2023)

Start-ups then have a choice. Go public and compete with these tech behemoths or sell yourself to them and grow within their ecosystem backed by their enormous resources. No wonder many start-ups decide to sell themselves to large incumbents. And that, in turn, has a chilling effect on VC investments in start-ups in these sectors. I have discussed how large tech companies create a kill zone around them where nothing new can grow.

Of course, that is not the only reason why companies are increasingly reluctant to go public, but in some sectors, it contributes to the problem. But if there is any good news coming out of the last two years of rising interest rates, it is that these tech mega-caps are increasingly strapped for cash and can’t just buy any new start-up anywhere.

In 2022 and 2023 the opportunity costs of going public have declined and that means that we are more likely to see good start-ups come to the public market again.

A good read. I think the governance burden is another contributing factor: maybe the same reason that over the last 18 months we've seen more public companies go private than we've seen IPOs. Public companies are subjected to a host of administrative and reporting burdens (e.g. SEC filings, Sarbanes-Oxley and FINRA compliance, quarterly "proctological" exams by Wall Street, etc.) that a private company can largely avoid.

Also, from the selling shareholder's perspective, sometimes selling to a strategic or financial buyer can offer a better valuation leaving the public market (and all it's administrative hassles) as a market of last resort.

I thought I'd share some data, that we use in presenting the case for investing in late-stage private growth companies.

Back in 1999, the average of a company before IPO, was 4 years and a market cap of $493m. In 2022 the average age of the company is 12 years and $2.393bn.

Historically, the average amount of companies that exit via M&A is around 55-70%, the rest is via IPO.

What we're also noticing is that more recently the so called liquidity premium is actually a discount, depending on the company and sector.

Post the JOBS Act, there's no real reason for a company to go public until they've reached true maturity, if ever. There is an abundance of capital in private markets, that wasn't there 10 years ago.

Of the US companies generating $100m+ in revenue, 74% of them are private.

Also, VC investors want to extract as much of the growth out of the company before dumping it on the retail investors.

I'd also disagree about going public and competing with the behemoths, the true battle is with Wall Street that like consistent quarterly earnings, no irregularities etc. If there's anything unusual the stock is dumped quicker than crypto scam.