ESG investing after the war

With the Russian invasion of Ukraine, ESG investing has taken a back seat, particularly when it comes to investments in defence and fossil fuel. Throughout the year critics of ESG investing have been pushing hard to reverse the advances of the last decade. What does that mean for investor portfolios as we head into 2023?

In 2020, as the Covid pandemic hit, some people tried to promote ESG funds as the better investment strategy because they significantly outperformed conventional funds. As I have written back then, this claim was built on sand since ESG funds tend to have a significant overweight towards technology stocks and growth stocks in general. This systematic bias came back to bite them in 2022 when growth stocks underperformed, and energy stocks rallied. The result was that while all equity funds suffered significant outflows in 2022, funds with a higher sustainability rating suffered larger outflows than funds with lower ratings, as researchers from the University of Exeter report.

Outflows from US equity funds with different sustainability ratings from Morningstar

Source: Chen et al. (2022)

Their analysis also shows that once you take fossil fuel stocks and defence stocks out of the mix, funds with high ESG ratings did not perform any different from conventional funds and within the sustainable funds' world, funds with a higher sustainability rating did not underperform funds with a low sustainability rating.

But we can’t take defence stocks or fossil fuel stocks out of the mix, can we? And clearly, these two industries have done really well in 2022. The problem just is that investing is forward-looking and I wonder if going into 2023 investments in fossil fuel stocks will be that great.

But let’s first look at defence contractors. In late 2021, there have been anecdotal reports of defence contractors having problems getting loans from banks as they tried to shun these investments for ESG reasons. This is why exclusions don’t work, part 1,428. Excluding industries from your portfolio not only makes your portfolio less efficient but also creates all kinds of unintended consequences.

Luckily, we have seen a change of hearts from banks and investors this year and more and more of them allow defence contractors back into their portfolios. As we prepare for a world after the Ukraine war, one thing seems obvious: All countries in Europe will have to spend more on defence. And that means defence contractors are moving into a secular bull market. And in my view, there is nothing wrong with investing in defence stocks as part of a sustainable portfolio. Being able to stand our ground against Russia and other authoritarian countries is part and parcel of creating a more sustainable future for all of us. Democracy and freedom are the foundation on which our efforts to shift the global economy rest. Do you think Vladimir Putting or Mohammed Bin Salman care about reducing greenhouse gas emissions to fight climate change? Or about increasing diversity?

But while I am convinced that defence contractors can and should be part of an ESG portfolio, I am not so sure about the fossil fuel industry. The advocates of a new commodity supercycle have come out of the woodwork in 2022 arguing that we will see another decade of rising prices for energy and metals. I really don’t know where that should come from in a world where Chinese demand is systematically slowing down, the US is hardly accelerating its efforts in building infrastructure (green or otherwise) and Europe is accelerating its transition to green energy in an effort to become independent of Russian oil and gas. Once we have become independent of Russian fossil fuels in a couple of years, what do you think will happen to the prices of oil and gas? What do you think will happen if Iran and Russia are allowed to export their fossil fuels to Europe again?

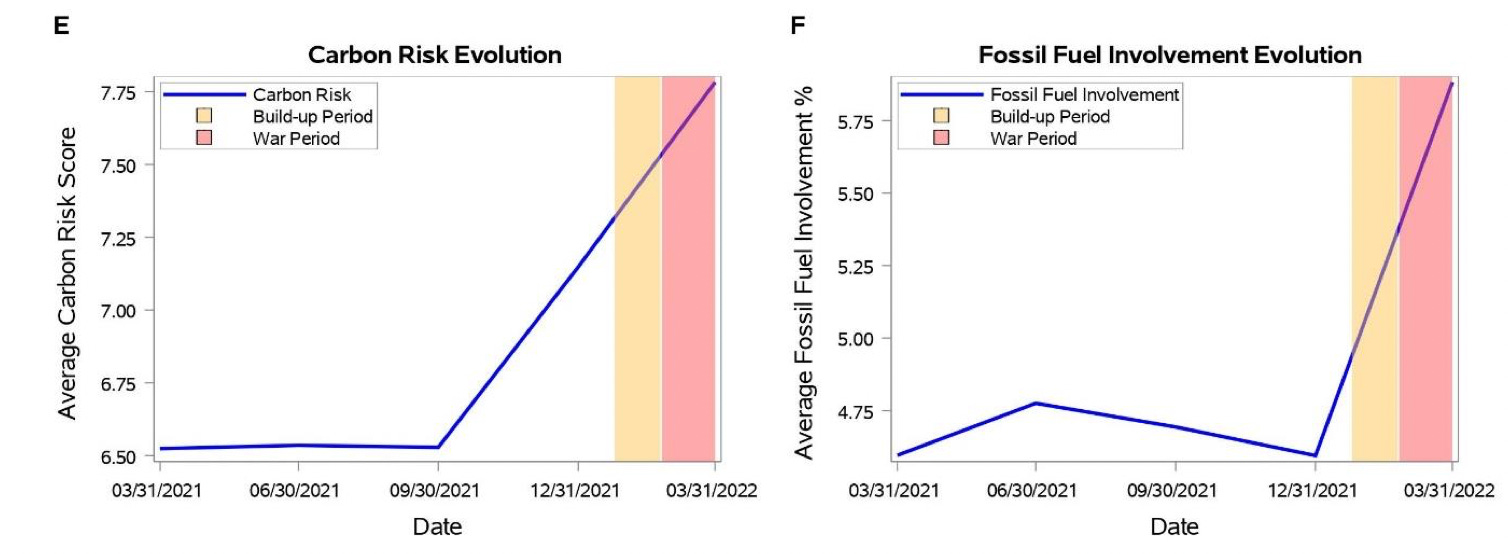

In fact, as the world heads towards a global recession, we have already seen oil prices drop from $120/bbl. in March to $80-90/bbl. today. Demand is declining and with it the prices for fossil fuels. Yet, the exposure of investor portfolios to fossil fuels has gone through the roof in the weeks after the Russian invasion of Ukraine. If it is not reduced in time, investors risk losing their profits for 2022 in the coming year.

Exposure to carbon risks and fossil fuels in US equity funds

Source: Chen et al. (2022)