Germans are bad at investing

I mean really bad. So bad indeed that one has to wonder what is going on there. And I know what that says about me as a German working in the investment industry. But let me explain…

There is a bit of a conundrum when it comes to Germans and their living standards. On the one hand, Germans are famously productive and inventive, creating a lot of income from their economic activities. Also, Germans are famously frugal with a rather high savings rate (particularly when compared to Americans or Brits).

But when one looks at living standards, the Germans typically lag the Americans and are not that much ahead of the Brits, French or other nations. In theory, if you have higher income and higher savings you can invest these savings and let the money work for you so that you end up with even more savings and higher income and thus higher living standards. Unless you do not make your money work for you…

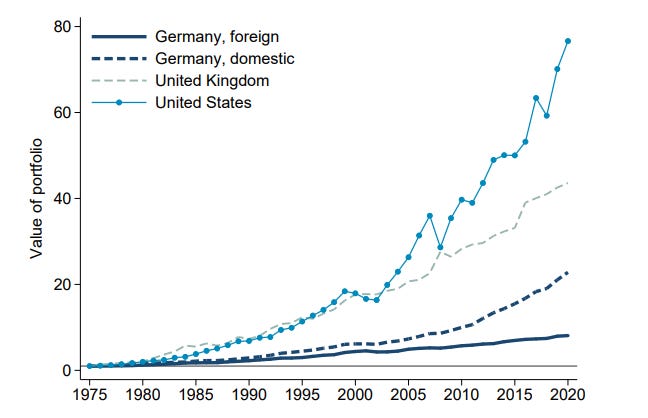

I know I am mixing things here that aren’t the same but stay with me for a minute and look at the chart below which is taken from an analysis by the Kiel Institute for the World Economy. It shows the cumulative return on German domestic and foreign investments as well as the foreign investments of the UK and the US.

Cumulative return of German, UK and US foreign investments

Source: Hünnekes et al. (2023)

The chart above shows that German foreign investments are not only worse than their domestic investments but miles behind the UK and the US. Now, be aware that this is the cumulative return of all kinds of foreign investments, which includes foreign direct investments, foreign portfolio investments in stocks and bonds, central bank reserves invested abroad and other investments such as trade credit.

But, and this is where things become relevant to most readers, one can show the same by just looking at equity funds located in different countries that invest abroad. Here is the average performance of international equity funds from 2000 to 2021 by location of the fund. German fund managers have among the lowest average returns and much lower average returns than their peers in the UK or the US.

Average international fund returns by fund country of origin (2000-2021)

Source: Hünnekes et al. (2023)

What is going on here?

The analysis of the Kiel Institute shows that these exceptionally low returns of German foreign investments have several sources:

German foreign direct investments are exceptionally low because Germans focus on investing in countries that are highly developed and ‘safe’ but have low growth rates and similar demographic problems as Germany itself. This reduces the average return compared to the foreign direct investments of other countries.

Among portfolio investments, Germans hold less equity and more bonds, thus creating lower returns through a more defensive asset allocation.

Within equity investments, Germans underperform markedly with their investments in technology and manufacturing as well as services.

Additionally, German equity funds are particularly bad at market timing, with less exposure during bull markets but similar exposure as investors from other nations during bear markets.

If you take a look at these drivers, you can find one common factor determining these decisions. Germans seem to have a generally lower risk appetite than investors in other countries. Germans are famously pessimistic, always expecting the next crash or bear market and this has significant consequences for their investments. As I have explained in my series against Cassandras, being pessimistic costs you a lot of money in the form of missed returns.

And because Germans are so incredibly safety-oriented and risk averse, they work hard but have less to show for it than the Brits or the Americans.

Which brings me to my own development as an investor. As an investor, I tended to worry all the time about things that could go wrong. And just like so many investors who worry too much I tended to sell out of a bull market too soon, missing out on a lot of the upside. It was only when I learned to stop worrying and learned to love momentum that my performance got better.

This is why I am on a mission to educate investors against the evil that are Cassandras and doomsters and why I insist on being optimistic as my default setting changing to a more pessimistic stance only when I have significant evidence that things could go wrong. Because if you are not, you are going to pay for it dearly, just like the average German does.

The German guy who founded a company for which I used to work used to say "Germans are great savers, and great speculators, but lousy investors". I've observed that I am only ever pumped for stock tips by the locals very close to market tops (in fact, I view it as a useful contrarian signal) ... it makes me want to say "well where were you five or 10 years ago?" Then people pile in at the top, and usually into a handful of high-flying single stock names instead of into a broadly-diversified index fund, and then they inevitably get crushed, which reinforces the bad societal vibes on equities ... how many Germans are still carrying a 77% top-tick loss in Deutsche Telekom stock nearly a quarter-century later https://www.google.com/finance/quote/DTE:ETR?hl=de&window=MAX ?

Take a look at a "Bierdeckel" I saw in Frankfurt in 1999 https://1drv.ms/f/s!At9od58qwtRejZBA7omWkC0gw5rfEg . The way German media portrays people involved in the stock market as constantly jumping up and down and/or running around with their ties flapping in the wind behind them is something one doesn't see anywhere else. This isn't a game :-( I was shocked to learn that in Germany, land of needing a license to go golfing, that there's no security licensing requirment as in the US with the Series 7 and UK via the FSA, so kids are plopped in front of telephones to start smiling and dialing on their first day at work. This all contributes to a general public cynicism about the investment business ("investment products are sold not bought").

I think one of the chief contributing factors to the phenomenon you describe is that Americans have self-directed 401k plans, and the British have ISAs, but the attempt at "Riester Rente" in Germany was a flop ... nothing gets one more interested in long-term investing than having some "skin in the game" with a substantial portion of one's own retirement funds. German treatment of investment gains at 25% "Abgeltungsteuer" for everything should make equity investment very attractive, but the German government's insistance on complicated tax calculation as one goes rather than just allowing things to compound up and then taxing it on withdrawl is a serious impediment to building real wealth. Another issue might have been the historic domiciling of brokerage accounts at banks rather than brokerages, and the resulting extraordinarily high fee levels. Before my local German bank kicked me out for being American, they offered to set up a special managed account (which turned out to be pretty much the DJIA), and with a straight face said they'd only charge me 3.5% (!) per year to do so. German retail mutual funds routinely have 150-175bp fees and relatively low-hurdle performance fees (sometimes booked on the first day of the year), which soak up realistic annual investment returns but quick. Finally, people are so over- focused on tax avoidance that they ignore Warren Buffet's famous warning "More investment sins are probably committed by otherwise quite intelligent people because of "tax considerations" than from any other cause.” I'd rather pay 25% flat on a 10-12% average annual equity return than stick my money in some "insurance wrapper" bond thing that turns out to be tax-free but with an effective yield of 1-2%.

There is a great quote from 'The Big Short' which amused me after watching WestLB/Dresdner/Commerzbank

...the folly of subprime mortgage investors, some large number of whom seemed to live in Dusseldorf, Germany. "Whenever we'd ask

him who was buying this crap," said Vinny, "he always just said,

'Dusseldorf.'" It didn't matter whether Dusseldorf was buying actual cash

subprime mortgage bonds or selling credit default swaps on those same

mortgage bonds, as they amounted to one and the same thing: the long side of

the bet.