Against Cassandras: The performance impact of Cassandras

I have discussed several common themes promoted by Cassandras and doomsayers over the past couple of weeks and why I think fears about these issues are overblown:

They may come to pass, but I think it is unlikely that they will. But of course, these themes tend to be tail risks. If they materialise, the damage to investment portfolios will be large, so even if they have a small probability of happening, isn’t it worthwhile listening to these Cassandras to prepare for such events?

The argument about the usefulness of tail risk hedging has been going on for decades and reasonable people can come up with different conclusions, but in the opinion of your humble writer, the performance track record of tail risk strategies is so poor that you would be ill-advised to even think about hedging such extreme events.

I want to make my point both with the help of a practical example and a simulated performance. First, let’s look at a fund manager who has become famous for hedging his portfolio in the run-up to the 2008 financial crisis and not losing money for his clients during this fateful episode.

John Hussman has been running his Strategic Growth Fund for more than two decades. His fund tries to beat the S&P 500 through two components. First, he is a traditional stock picker, selecting stocks in the US that he thinks will outperform the index overall. Second, he can temporarily hedge all or parts of his portfolio against downside risks through the use of derivatives. Before 2008, Hussman was convinced that US equity markets were overvalued and he hedged his portfolio against downside risks, which is why he was so successful in preserving capital for his investors.

Unfortunately, Hussman has been convinced since 2010 that US equity markets are overvalued once again. By 2020, with the onset of the pandemic and then the bear market of 2022, one could argue, Hussman has eventually been proven right. So how did his fund perform? The chart below shows the performance of the Strategic Growth Fund taken from Hussman’s home page. He shows the performance of the S&P 500 together with his portfolio of selected stocks (i.e. his track record as a stock picker) and the performance of the portfolio with tail risk hedges. As you can see, Hussman is a good stock picker and has outperformed the S&P 500 by a significant margin before the tail hedges were implemented. Unfortunately, his clients didn’t get to enjoy this performance, because what they got by investing in the fund was the stock selection including the protection against downturns in expensive markets. And that performance isn’t pretty. Over the three years ending 28 February 2023, the annual return of the Strategic Growth Fund was 6.95% compared to 12.15% for the S&P 500. Since the inception of the fund, the annual return of the fund was 0.99% compared to 6.54% for the S&P 500.

Performance of Hussman Strategic Growth Fund

Source: Hussman Funds

But I don’t want to pick on John Hussman. He is a fund manager who I admire for his intellectual prowess and who does his best and puts his money where his mouth is. And that is much more than can be said of all the doom and gloom prophets who write investment letters but never show the performance of their recommendations or who sometimes even invest in contradiction to their pessimistic outlook.

So, let us look at a more systematic analysis of tail hedging strategies done by Roni Israelov and David Nze Ndong. They looked at the performance of three different ways to protect a portfolio against extremely unlikely but potentially severe losses and how they performed in the years of the Covid pandemic and the bear market of 2022. To be precise they looked at a simple put protection strategy where investors buy the S&P 500 together with out-of-the-money put options as a first strategy. The second strategy was to buy straddles and strangles that allow gaining long volatility exposure (something akin to what many hedge funds do to hedge tail risks). And finally, they tested a simple strategy of going long VIX futures.

In the end, they found that neither of these tail hedging strategies worked well over the 2020-2022 period despite markets going through the worst turmoil since the financial crisis. In fact, the authors note that the performance of the different tail hedging strategies varied by a large amount and was timing and path dependent. In other words, if you can time the markets well, tail hedging can be profitable. To which I say that if you can time the markets well, you don’t need tail hedging because you can simply sell your stock holdings and then buy them back when the turmoil is over…

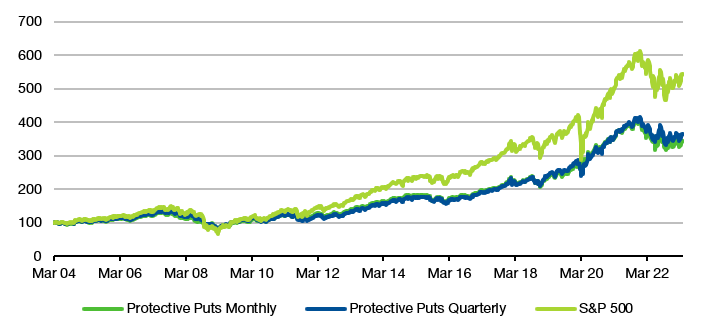

To give you an example of what these tail hedging strategies do to a portfolio take a look at the chart below. It shows the total return of the S&P 500 together with two put protection strategies. The monthly strategy buys 5% out of the money puts every month, while the quarterly strategy buys 10% out of the money put options that expire every quarter. So, you are protecting your portfolio every month or quarter against large losses. Here is the performance since 2004:

Protective put strategies since 2004

Source: Liberum, Bloomberg

The average annual return of the S&P 500 since 2004 was 9.2% compared to 6.6% for the monthly put protection strategy and 7.0% for the quarterly put protection strategy.

Even if you somehow had the genius to not hedge your portfolio until the start of 2020 and then implement the put protection and keep it in place until today, you would have lost money compared to just holding the S&P 500. And that is in a period when we had the worst pandemic in 100 years and a bear market in the S&P 500 as well as a spike in inflation to 40-year highs. In fact, the outperformance you accumulated during the pandemic year 2020 was gone by mid-2021. In order to make money, the Cassandras would have to be able to time both the start and the end of the pandemic with very high precision.

Protective put strategies since 2020

Source: Liberum, Bloomberg

In sum, if you listen to Cassandras, I am very confident, you will lose money in the long run. The only way to make money with doom and gloom forecasts is to time them both on the way in and on the way out very precisely. And I know nobody, who can do that. In fact, the simple observation that the Cassandras all seem to be bearish all the time should tell you one thing: The only ones making money from these doom and gloom forecasts are the ones who make them.

Back in my dim and distant past I worked at a bank where the equity strategist collaborated with a professor to write a long paper showing comprehensively that systematic hedging with put spreads doesn’t work. Much like the paper you quote here. My boss (head of derivatives sales) was furious. I was tasked to write a rebuttal, which I did. Almost 20 years later I still stand by my conclusion: systematic hedging strategies don’t lose money because they are wrong, but because they are lazy. It boggles my mind that people who think deeply before they choose to invest then abdicate all thought before hedging. The Price — and hence the Value — of hedges change all the time. If you don’t heed this simple rule of markets you’ll lose money. Whether you “invest” or “hedge”.

I’m also amazed analysis of systemic strategies in academia is still a thing. Shame on professors.

I have really enjoyed your “Against Cassandras” series and have taken it as motivation to go after the commercial real estate Cassandras that are prevalent today. It seems only fitting since I spent over ten years trading distressed CMBS through the aftermath of the GFC and have become somewhat knowledgeable of the broader CRE industry. In general Cassandras are linear thinkers, whereas most problems are non-linear by nature.