The chart that haunts me

The chart below has haunted me for the better part of 2019 now. It shows the consumption per capita in the US and the UK by age as recorded by the National Transfer Accounts Project. In order to make the data more comparable, I have normalized it in such a way that the consumption between age 20 and 64 averages to 100%.

Consumption per capita by age

Source: National Transfer Accounts.

There are so many fascinating insights into these curves. For one, it shows that all the people who warn that with the retiring baby boomer generation, consumption should enter a secular decline might be wrong. Yes, older people consume less, but only when they get much older. In the first ten years of retirement, they consume more than before. This means that as the baby boomers retire the demographic shift isn’t going to create a slow-growth economy due to declining consumption. Instead, consumption is likely to pick up for a while compensating to some extent the decline in investments and productivity we have witnessed over the last decade.

This also means that there are lots of investment opportunities out there for people who want to benefit from this increased consumption of early retirees (that is people aged between 60 and 75 when consumption per capita is highest). Their consumption patterns change relative to working-age people insofar as they spend more on recreation like travel, sports, eating out, etc. I have discussed here that this creates challenges for retirement planning, but for investors in companies that provide these goods and services, it is a boon.

The investment opportunities that are typically discussed when talking about retirees and an aging population are cruise companies like Norwegian Cruise (NCLH) or Carnival (CCL), and healthcare property investments like Assura (AGR) or Universal Health REIT (UHT). Furthermore, investors like to invest in pharmaceutical companies with blockbuster drugs against Alzheimers or Parkinsons. But not too many investors think about the opportunities in providers of services like sporting goods, like Callaway Golf (ELY) or Brunswick (BC). Or think about builders of boats and other recreational vehicles like Malibu Boats (MBUU) and BRP (DOO). These are companies that are going to benefit over the next five to ten years from the demographic shifts as the baby boomer generation retires, long before these people need Alzheimer’s drugs and a place in a nursing home.

The second thing that always intrigues me about the chart above is the massive increase in consumption expenditures in the US compared to the UK at very old age. This increase in consumption in the US is unique insofar as it does not appear in any other developed country. I have speculated from the first time I built this chart that it might be due to rising healthcare costs in the US. In the UK, as well as in most other developed countries, healthcare costs are kept in check by a combination of universal health insurance that ensures that drug companies have to negotiate prices with the local government as the main insurer as well as price controls that are not only in place in socialist democracies like Sweden, but also in liberal countries like Switzerland. And with their extremely low tax rates and the absence of a government health insurance (there is a mandate to have health insurance, but the insurance is private insurance) the Swiss cannot be considered socialist. Yet, the Swiss government realized that in order to make private health insurance affordable for everyone, they needed to regulate prices.

None of these price controls for health insurance, drugs, and other medical services exist in the US, which is why I thought, consumption starts to rise so dramatically at old age when physical decline sets in and health care becomes a bigger and bigger part of the personal consumption basket.

Luckily, I no longer have to investigate this hypothesis myself since James Banks and his colleagues from the Institute for Fiscal Studies in the UK and the RAND Corporation in the US have done exactly that. They looked at the big divergence in consumption spending (in their case they looked only at nondurable consumption spending that shows a similar divergence) and tested several explanations for it. For example, in the US, households are much more likely to downsize after retirement and move to a different part of the country than in the UK. Maybe, after downsizing, the pensioners simply like to spend more on vacations and entertainment than before? Maybe the divergence has its roots in different incomes generated before and during retirement since it is much rarer for pensioners in the UK to continue to work than in the US?

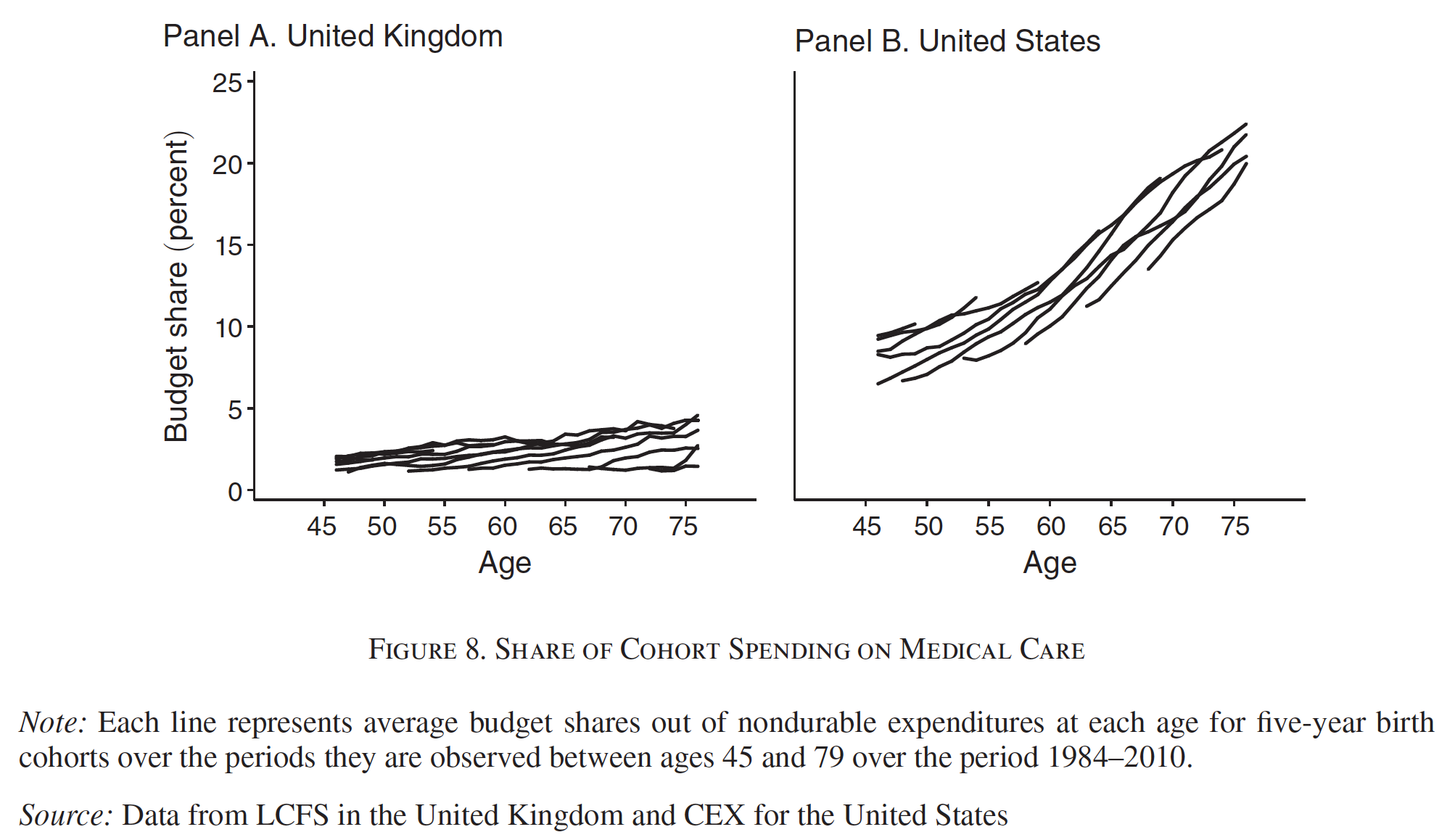

But of all the different explanations they investigated, only one could explain the divergence: health care. The fast-rising health care costs in the US and the need to create an emergency pool of money to cover out of pocket payments and other health care payments in the US creates a much higher need for Americans to spend in old age. The chart below provides the key insight. It shows the share of the personal expenses allocated to health care. In the US it is not only about five times higher than in the UK, where the National Health Service provides free health care to virtually everyone in the country. It also rises much faster in the US and eventually reaches about a quarter of all nondurable expenses at high age. And this is despite the fact that in the US, Medicare is available for people above the age of 65 as a healthcare system.

That Americans are not up in arms about this is a mystery to me. Think about it this way: Instead of being able to inherit your lifetime savings to your children and grandchildren or donate it to charity for a good cause, the pharmaceutical industry and health insurance industry is taking the money away from you. It is like an extra 25% estate tax levied on everyone, rich and poor alike.