The Virtuous Investor: Rule 1

Fight the evil of ignorance – knowledge is the foundation of success

This post is part of a series on The Virtuous Investor. For an overview of the series and links to the other parts, click here.

“Let it move thee nothing at all that thou seest a great part of men so live, as though heaven and hell were but some manner of tales of old wives, to fear or flatter young children withal: but believe though surely and make no haste, though the whole world should be mad at once, though the elements should be changed, though the angels should rebel: yet verity cannot lie.”

Erasmus of Rotterdam

Just like the virtuous Christian needs to know the true God, so too must the virtuous investor know the truth about financial markets. The problem with investing is that there are plenty of folk tales and rules of thumb that make the round that are either flat out wrong or no longer true.

Take retirement planning for instance. It used to be a good rule of thumb to say that your living expenses after retirement will be about 80% of your living expenses before retirement. Your house will hopefully be mortgage-free by then, your children will be out of the house and no longer need financial assistance and your lifestyle will become somewhat more sedentary.

However, this is the 21st century and things have changed. People have children later in life and their children live with their parents way past the moment they leave school. And they need their financial support for longer. When I was born in 1974, the average age of a mother in England was 26.4 years and 29.4 years for the father. In 2016, the average age of a mother had risen to 30.4 years and for a father to 33.3 years. And the think tank Civitas estimates that in the late 1990s, 19% of 20- to 34-year olds in the UK were living with their parents. In 2017, this share had risen to 26%.

Put together, this means that parents have to financially support their children longer and to a higher age, preventing them from saving for retirement and reducing their expenses after retirement. In fact, the chart below shows the average consumption of people in different countries as a function of age. I have normalised the data in such a way that it averages to 100% for ages 20 to 64. Values above 100% indicate higher living expenses than during the working years of your life. As you can see in all the developed countries shown in the chart, consumption increases by about 20% in the first ten years of retirement. The reason for this phenomenon is that, yes, people have more disposable income since they have paid down the mortgage on their house. But instead of cutting back on expenses, they tend to spend that extra money on travel, hobbies, sports and other things. As well they might. They have worked hard for that money and good on them if they enjoy life after retirement. But don’t enjoy retirement and still use a replacement ratio for your retirement plan of 80%, because that number has become totally unrealistic in today’s world.

Consumption rises after retirement

Source: National Transfer Accounts.

Using wrong or outdated rules of thumb can be worse than using no number at all. After all, a little knowledge can be a dangerous thing as Alexander Pope already knew and as I have discussed here.

The foundation of investment success is accurate and up-to-date knowledge. Knowledge about markets, financial products and services, fees, and all the other things that influence your investment decisions and the outcome of your decisions. Let’s stay with the challenge of retirement planning. Annamaria Lusardi and Olivia Mitchell showed in an influential study that better financial knowledge leads to higher savings ratios and increased wealth in old age.

In their study, they tested if people understood simple financial concepts such as inflation, compound interest and diversification of risks between stocks. They also asked if people had a retirement plan in place and what kind of a plan this was, ranging from no plan to a simple plan (e.g. I need to save x% of my income for retirement) to a fully-fledged plan they successfully implemented. They found that only about one third of US households got all three questions on financial knowledge right and only about one third of the population had more than a simple plan for retirement in place. The correlation between high financial literacy and having at least a simple retirement plan in place is high, i.e. people who know more about basic investment concepts also are more likely to have a financial plan for retirement.

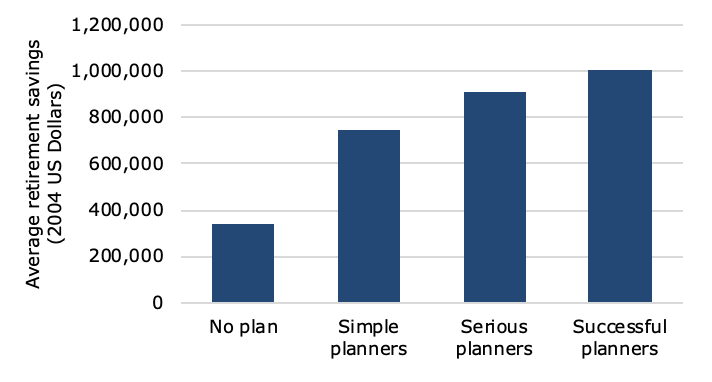

And this financial plan pays. The average wealth of households who did not plan for retirement in 2004 was $338,418, while successful planners had almost three times as much money in their nest egg at $1,002,975.

Average retirement nest egg for Americans

Source: Lusardi and Mitchell (2011).

The link between financial literacy and financial success is by now well-established. People who have a higher degree of knowledge about financial markets and investment basics, such as the three topics mentioned above tend to participate more often in the stock market and invest more in stocks. And since stocks in the long run have higher returns than bonds or money market investments, these investors tend to have higher returns as well, simply by being in the market.

Unfortunately, most people are not very knowledgeable when it comes to financial matters. Study after study shows that only about half of the population understands concepts such as inflation and compound interest and only about one third of the population have sufficiently broad financial knowledge to answer a wide range of these basic questions correctly. Literacy is particularly low for women, the less educated and racial minorities. This creates a vicious cycle. Poorer people tend to be less knowledgeable about investment matters. Because these people are less knowledgeable about investments and basic financial concepts, they tend to invest less and in the wrong financial instruments and products. And because of that, they will fall even further behind the people who invest more and in better performing assets and products.

The financial industry is full of advisers who only care about selling product. They prefer their clients to be less knowledgeable so they don’t ask too many pesky questions about fees or the risks of an investment. But pushing product is an unsustainable business model. First of all, regulators increasingly crack down on advisers who sell unsuitable products to clients. And efforts to block the general introduction of the fiduciary standard in the US notwithstanding, the fiduciary standard is increasingly adopted as a requirement for advisers around the world. This means that advisers have to put their clients’ interest above their own and cannot sell any product that is “suitable” for the client, no matter if there is a better product available.

Part of living up to the fiduciary standard is, in my view, the necessity to educate clients. Increasing client knowledge about all kinds of investment related topics might not make them better at mathematically challenging concepts such as compound interest. Research on financial literacy education has shown that people don’t necessarily get better at answering these questions after being educated about them. But their attitude towards investments changes. They become less afraid of the complexities of the investment world and more interested in the mechanics of it. As a result, their participation in equity markets tends to increase and their investment behaviour changes. Increased knowledge leads to more and better interaction with markets and this, in turn, creates a virtuous cycle where people become more and more engaged and learn more about investments, which in turn increases engagement etc.

Thus, financial knowledge is the starting point of the virtuous investor. Without it, markets seem scary, with it, markets become interesting. And with increased interest come increased participation and better decisions.

The virtuous investor tries to learn as much as possible about markets, products and investments and this learning process never stops but turns into lifelong learning. The virtuous adviser, on the other hand, educates his clients and encourages this accumulation of knowledge and lifelong learning.