The Virtuous Investor: Rule 3

Analyse your fears – they will lead you astray if they can

This post is part of a series on The Virtuous Investor. For an overview of the series and links to the other parts, click here.

“Set this third rule before thee alway, bear thyself in hand that all the fearful things and fantasies which appear forthwith unto thee as it were in the first entering of hell ought to be counted for a thing of nought.”

Erasmus of Rotterdam

Every investor will experience losses from time to time. It is unavoidable unless you keep all your investments in cash and money market investments, but even then, you might experience the loss of purchasing power (though these losses are less salient than losses in the market value of securities). Unfortunately, behavioral finance has shown that we fear losses more than we value gains. If you have savings of £100,000 and you lose £10,000 this loss weighs about two to three times as much as a gain of £10,000. It is this fear of losses that leads us astray as investors and tempts us to change our investment strategy too often, as I have written in Rule 2. But this fear of losses also gives rise to the equity risk premium and the fact that equities have much higher returns than bonds or bills.

But the third rule of the virtuous investor is not just concerned with loss aversion and fear of losses in general. As it says, “analyse your fears” it is important that everyone of us understands their individual fears.

What is it that leads you astray in your investment decisions?

In my view, there are three sources of our fears:

Our genetic make-up and predisposition

Our cultural background and the environment we live in

Our individual experiences

Amir Barnea and his colleagues have exploited the rich data of the Swedish Twin Registry to assess the importance of these three factors in explaining the variation in equity holdings of Swedish investors. The chart below shows the key result from their study.

Variation in equity holdings explained by genetic influences as well as collective and individual experiences

Source: Barnea et al. (2010).

The first thing to notice is the surprisingly large influence of our genes. Our genetic make-up can explain about 40% of the variation in the riskiness of investor portfolios for young investors, but even at high age, the genetic make-up still explains about one fifth. Studies by Camelia Kuhnen and Joan Chiao as well as Anna Dreber and her colleagues could trace this genetic effect back to the dopamine receptor D4 gene (DRD4). Now, it is up to you if you want to get a genetic testing kit to check if you are genetically programmed to be more risk averse or not, but there is a simpler way to assess if you are.

Just like doctors go through your family history to check if you are at risk of certain types of cancer, so you can go through your family history to check if you are more prone to risk taking or not. We know that children of entrepreneurs are more likely to be risk-takers and become entrepreneurs as well. Similarly, if there is a preponderance of people in your family with jobs that incur significant financial risks (stock broker comes to mind) then it is an indication that you might be carrying the risk-taking version of DRD4. On the other hand, if your family members are all civil servants, teachers and other employees in relatively stable and secure jobs, it seems likely, that your genetic make-up is tilted more towards the risk-averse type.

The second source of our fears is the shared environment we grow up in. Younger investors are apparently influenced to some extent by the cultural background they grow up in. Studies have shown that Germans, for example, are more afraid of inflation risks and on average less prone to own their house (and rent instead) than Americans. More generally, investors who live in more individualistic societies tend to be more risk averse than investors who live in more collectivist societies like China, where the safety net provided by family and distant relatives provides a safety net in case a person falls on hard times financially. However, these cultural influences are typically small and decline to zero as an individual gains more experience as an investor.

The one exception to this rule seems to be the “keeping up with the Joneses” effect that states that we are constantly trying to keep up with our neighbors and friends. Harrison Hong and his colleagues have shown that this not only influences our preferences, but also our “fears”. If you live in a community where fewer people invest in the stock market, you are also less likely to invest in the stock market. On the other hand, if you are more sociable and outgoing, you are more likely to invest in stocks, while less sociable people tend to be less prone to invest in the stock market.

But the chart above makes it clear that the most important source of our fears are our individual experiences. And here, the formative years between age 16 and 25 tend to have a lasting influence on our investment decisions. Studies have shown for example that our attitudes towards recessions and inflation are shaped to a large extent in our formative years and these memories influence our investment decisions for life.

One of my first experiences as an investor was to buy a mutual fund specializing in technology stocks in 1998. I was at the time working in an IT company and got swept away in the enthusiasm for the new technological inventions like the internet. Plus, I knew what I was doing, because I worked in the industry which gave me a better understanding of the opportunities. Yeah, right. I finally sold the fund four or five years later with an 80% loss…

This formative experience with the tech bubble meant that I was from then on seeing bubbles everywhere and steadfastly refused to invest in tech stocks for many years. My individual fears were shaped by this traumatic experience in my formative years and it took a long time for me to overcome these fears. Today, I invest in technology stocks again and I am not afraid of bubbles that much – though I can still see them everywhere around me these days.

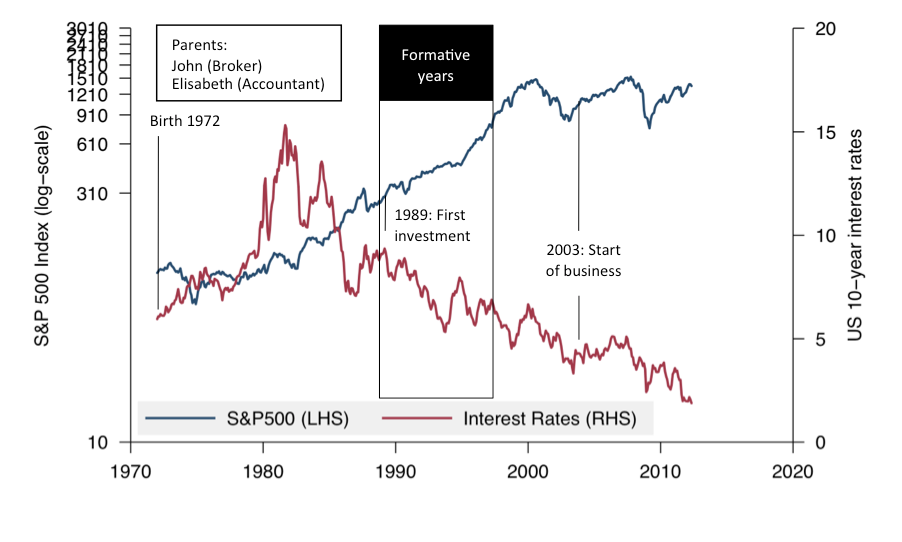

In a paper for the Journal of Wealth Management my co-author Robin Miranda and I discussed a simple technique to identify your individual fears that have been triggered by our experiences. It consists of drawing a timeline of your lifetime experiences next to the development of the stock market and interest rates in your home country. This way, you can immediately see the connections between your experiences and how they have been influenced by the overall market environment.

Below is an example of this tool for a 40-year old US entrepreneur. In this example, the entrepreneur made his first investment in the late 1980s and benefitted from the roaring bull market of the 1990s. Similarly, he experienced declining interest rates throughout his entire life and started his business in 2003 when interest rates were low and loans were cheap. These experiences have likely influenced this individual to not be afraid of inflation, stock market crashes or rising interest rates. As a result, the individual fears of this investor are likely to be very different from mine and we would probably make different investment decisions due to these differing experiences.

Recognising these differences in our fears is the first step to overcome them. Just like I managed to overcome my fear of bubbles and technology stocks, so you can overcome your fears and improve your investments.

The lifetime experiences of a 40-year old entrepreneur

Source: Klement and Miranda (2012).