A couple of months ago, I wrote about how bad Germans are at investing. One piece of evidence was that German business owners are bad at directing foreign direct investments (FDI) to high return places. Instead, they prefer to invest in regions that are safer and geographically closer to home. Now, a new study on the impact of the Trump Presidency, the pandemic, and the Ukraine war looks at how German FDI has changed in the last six years…

Germany famously is the Exportweltmeister (World Champion of Exports), and heavily depends on demand from foreign buyers for its high-tech goods. The result is that Germany’s outward-bound FDI is a good indication of future economic growth in Germany because so much of the German economy depends on trade links and supply chains to these export destinations.

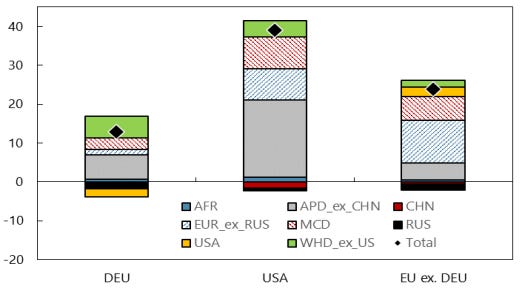

A team at the IMF has looked at German outbound FDI over the last six years from 2018 (the start of Trump’s trade war with China) to 2024. Here is the growth in outbound FDI from the pandemic lows in Germany, the US, and the EU ex Germany. Note that Germany’s FDI has rebounded much less than the rest of Europe or the US.

Growth in outbound FDI since the pandemic lows

Source: Fletcher et al. (2024). Note: AFR = Sub-Saharan Africa, APD ex CHN = Asia Pacific ex-China, CHN = China, EUR ex RUS = Europe ex Russia, MCD = Middle East and Central Asia, RUS = Russia, WHD ex US = Western Hemisphere ex USA.

A closer analysis of the change in outbound FDI shows that German FDI has not just been slow to recover, but increasingly focused on regions and countries that are closer to Germany from a geopolitical perspective. Investments in Russia and China but also the US have become incredibly sensitive to geopolitical tensions as German businesses are reluctant to invest in countries that may end up on a sanction list or be implicated in trade wars.

Instead, German businesses have kept their powder dry (there was no surge in domestic investments either) and in case of doubt invested in Europe ex Russia, Asia ex-China, and Latin America (from Mexico down to South America). What stands out to me in this picture is that Germany is trying to play it safe once again and – just like China – is trying to get low-tariff access to the US via investments in Mexico or Canada which are part of the USMCA free trade zone.

On the one hand, this behaviour is understandable in a world of increasing geopolitical uncertainty. On the other hand, it further reduces German returns on FDI and reduces the trade links to China, Russia, and the US. This will eventually translate into fewer exports and lower GDP growth.

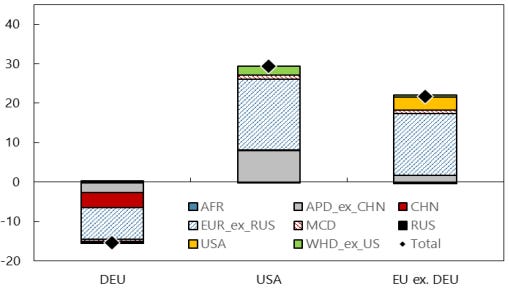

Now, let’s look at the inward FDI into Germany, the US, and EU ex Germany below since the pandemic.

Growth in inbound FDI since the pandemic lows

Source: Fletcher et al. (2024). Note: AFR = Sub-Saharan Africa, APD ex CHN = Asia Pacific ex-China, CHN = China, EUR ex RUS = Europe ex Russia, MCD = Middle East and Central Asia, RUS = Russia, WHD ex US = Western Hemisphere ex USA.

Germany has seen inbound FDI decline(!) since the pandemic, while the US and the rest of the EU have seen massive growth in inbound FDI. But inbound FDI means jobs created in Germany and additional domestic investments. This is a really scary chart if you live in Germany. It indicates that Germany will likely be hampered by very low growth in the next five to ten years and will once again be known as the sick man of Europe.

A lack of FDI in Germany is not the culprit, though. It is only a symptom of a lack of investment opportunities in Germany and an economy that is focussing too much on ‘old’ technology like internal combustion engine cars rather than EVs. Or chemicals and machinery rather than semiconductors and software.

For decades, Germany has been the economic powerhouse of the EU but now the country is stuck in a glorious past and has missed many of the shifts that will dominate the economy of the 21st century. Come to think of it, the only future technologies that I can think of where Germany is leading are renewable energy and industrial automation. Everywhere else, Germany is either a non-player (software, AI, data security, consumer tech) or trailing even its European neighbours (services, fintech, medtech/biotech, semiconductors, etc.).

I am confident that Germany will eventually focus on its strengths and will build a new economic powerhouse, but for the foreseeable future, I don’t think Germany will be able to compete with the rest of Europe, the UK, or the US. Germany had it too good for too long and now they have become fat and lethargic. Time to get back on the treadmill and get fit again, even though that may take a decade.

I recently did an article for a US magazine on how Germany's socio-economic system based on cooperation, consensus and social justice to serve the interests of multiple stakeholders - Rhineland Capitalism - e.g. Co-determination ‘Mitbestimmung’ approximated what Adam Smith originally wrote was a functional economy than US turbo charged shareholder capitalism. I shared it with a few of my German friends and they all commented how screwed the German system has become. Some suggested its corporate governance had lapsed, others suggested leadership...I was surprised because as an American Rhineland capitalism seems far superior and light years ahead in terms of a socio-economic model and an export juggernaut and Hidden champions are world beating. Has there been any systemic analysis on what's happened to the Rhineland model? My eldest daughter was born and raised in Berlin which is an amazing city full of start ups, edgy, ect and they are streets ahead of us on so many fronts, e.g. recycling and technical prowess. And their education system is awesome, and their vocational training seems second to none. So what's happened? This may not be the best forum as I'm sure it's a long and complicated story...