Demographics and inflation: I am not convinced

I have talked about my reluctance to invest based on demographic trends before. In almost all cases, trying to exploit demographic trends in your investments or even using demographic trends to forecast economic developments like growth or inflation is a fool’s errand. It sounds great in theory, but in practice, any demographic shifts are so small that they are easily dominated by cyclical developments.

Yet, it is at the beginning of 2021 that I find many people again being seduced by the siren song of demographic shifts. In recent weeks, I have seen economists argue that in 2021 and beyond, we should see inflation rise because the baby boomers are retiring and the millennials are starting to buy houses, etc. And of course, people argue that retirees save less and thus influence the aggregate savings and consumption in an economy, something that is not supported by the actual facts on the ground as I have written here.

One of the most prominent examples of the recent argument that demographics are going to change our world is the new book by Charles Goodhart and Manoj Pradhan. It argues that we are at the cusp of a major demographic shift that will lead to higher inflation, higher interest rates and lower inequality in the future, thus reversing three decades-old trends. If you are interested, there is a review of the book by Larry Siegel here. I have read both the book and the original paper it is based on and let me tell you a little secret. If you just read the original paper from 2017 available for free here, you can save yourself the money to buy the book.

The main problem I have with their argument is that most of it rests on the assumption that in an ageing society, we will get higher inflation. Even their call for higher interest rates indirectly rests on the assumption that inflation has to rise since real rates are likely to stay low or even decline from current levels (which, by the way, is something I agree with and is supported by tons of economic studies) at the short end of the yield curve. However, as they say in their book (p.99):

“In contrast, however, as this new, uncomfortable, world emerges into clearer sight, long rates will start rising and very likely rise above the current rate of inflation. So, one of our conclusions is that the yield curve, which is currently flattened to an unusual degree, will probably steepen sharply.”

Note, how the argument of a steepening yield curve rests on rising inflation and then nominal rates rising faster than inflation to generate higher real rates. There is a lot of handwaving going on here without any quantitative analysis if this assertion is really true.

Don’t get me wrong, I do think that inflation is going to rise in 2021 from the depressed recession levels of 2020 and as part of that trend we should see yield curves steepen even more than what we have seen so far. But that is not due to demographics.

In fact, I often tell people to show me a chart that shows a direct connection between demographic changes and inflation. I have yet to see one and Goodhart and Pradhan never show such a direct link either. The closest they come is Table 5.2 on page 85 of their book. There, they quote as they have done in their original paper, the work of Yunus Aksoy and his colleagues to measure the sensitivity of inflation changes to demographic changes.

The table below shows the sensitivities of inflation to changes in the population shares of three major groups, young people aged 20 and younger, working age people between the age of 20 and 59 and older people aged 60 and over. I show three different results because the sensitivities go through a bit of an evolution over time. In the original paper by Goodhart and Pradhan from 2017, they show the sensitivities in the top row. In their book, they quote the numbers in the second row from a 2015 working paper by Aksoy and colleagues, and the bottom row shows the number that Aksoy and his colleagues show in their final published and peer reviewed paper. Note especially, how the sensitivity of inflation to the change in older population declines by two thirds from 0.17 to 0.05 over different iterations of the research. And furthermore, Goodhart and Pradhan forget to mention in both their academic working paper and their book that at no point is the sensitivity to demographic changes of people aged 60 or over statistically significant. In fact, the correct interpretation of the results of Aksoy is that there is no link between demographic changes in older parts of the population and inflation. Even more so, Aksoy and his colleagues in their paper make no claims that an ageing society should lead to higher inflation. They show that there are statistically significant links between demographic changes and inflation (which is true for the young people and working age people but not older people), but they never mention older people as the driving force or claim that inflation should rise.

Estimated links between demographic changes and inflation

Source: Goodhart and Pradhan (2017), Goodhart and Pradhan (2020), Aksoy et al. (2015), Aksoy et al. (2018).

Be that as it may, let’s take the original numbers of Goodhart and Pradhan at face value since they should show the most inflationary effect of demographic changes. I have done the following calculus with all three assumptions and for three regions: the United States, the UK and advanced economies in general. If you want to check my work, feel free to email me and I will send you the Excel. In what follows, I will only show the United States for simplicity, but the results are pretty much the same in all three countries/regions and with all three assumptions from the table above.

First, let’s look at the size of the impact of demographic changes on inflation. I have used the same UN Population data that underlies the work of Goodhart, Pradhan and Aksoy et al. The UN provides this data in five-year increments and in lots of granularity by age. Below is the resulting cumulative impact over five years for the United States.

Projected impact of demographic changes on inflation

Source: Goodhart and Pradhan (2017), UN Population Division, author’s calculations.

First, note that the projected increase in inflation should have already happened in the last five years. The next five years will see a similar demographic impact on inflation as the period 2015 to 2020 before the demographic push for inflation declines again. Second, note how small the annualised effect of demographics is. Cumulative over five years, the model expects inflation to increase by 0.7%, or c.0.15% per year. That isn’t really a major force to influence inflation.

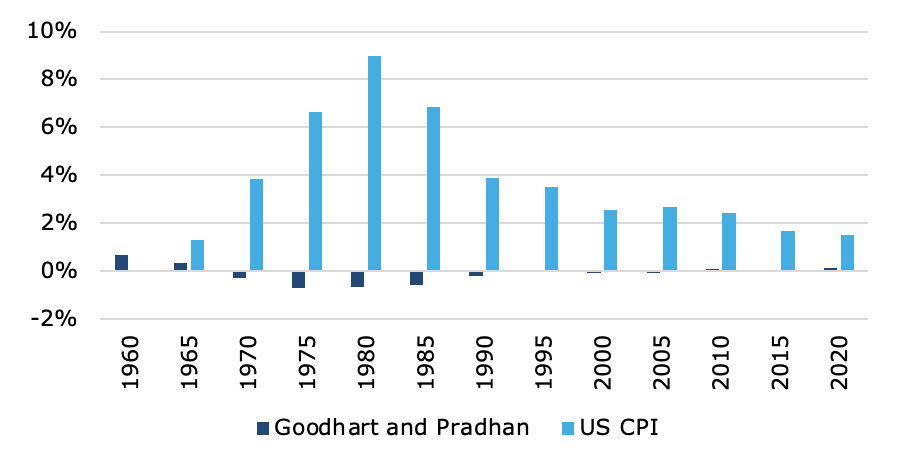

Next, let’s have a look at how this demographic influence on inflation compares to past realised inflation. After all, the model was built based on historic data so if it doesn’t work in the past, what hope is there for it to work in the future?

The chart below compares the demographic inflation impulse with the realised annual inflation in the United States in the corresponding five-year intervals. Note that since I use annual inflation rates, I compare them to the annualised demographic impulse on inflation.

US inflation vs. demographic impulse

Source: Goodhart and Pradhan (2017), UN Population Division, author’s calculations, Bloomberg.

There is clearly no connection between the demographic impulse on inflation and actual inflation in the past. In fact, the correlation between the time series is -0.94, indicating that inflation was higher in times when the demographic impulse was low or even negative and inflation turned out to be lower on average when the demographic impulse got larger.

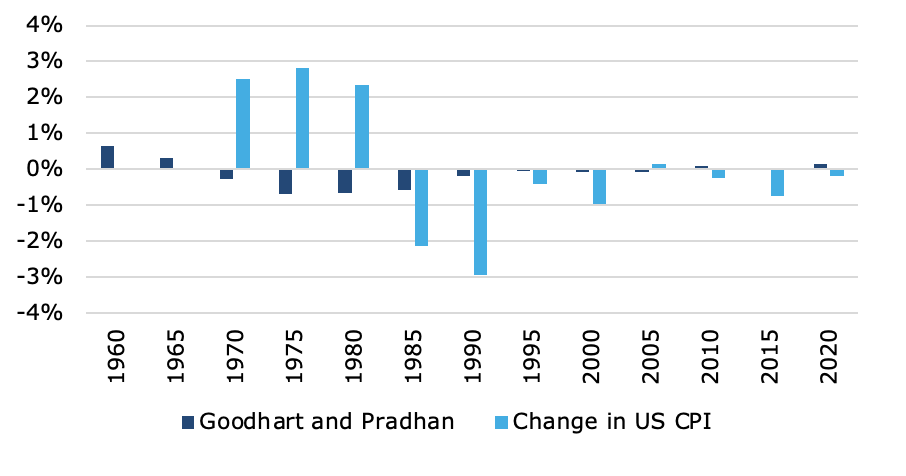

But then again, we are talking here about an impulse, so the demographic impulse should be more closely linked to changes in inflation levels rather than actual inflation. The chart below shows that comparison.

Change in US inflation vs. demographic impulse

Source: Goodhart and Pradhan (2017), UN Population Division, author’s calculations, Bloomberg.

Note how tiny the demographic impulse is in comparison to the actual change in inflation. And be aware that while the correlation between demographic impulse on inflation and changes in inflation is better, it still is -0.41. Or in other words, when the demographic impulse to inflation was negative, the 5-year average in inflation went typically increased and when the demographic impulse was positive, inflation went down. Out of 11 5-year periods, the demographic impulse has the same direction as the eventual shift in inflation only in 4 out of 11 cases. A flip of a coin would get the direction of change in inflation right more often than that.

Remember, how I told you I have never seen a chart showing direct evidence that in an ageing society, inflation has to increase? Well, the two charts above are the reason why because they are these charts that you never see. They are the direct link between demographics and inflation. And to me, the evidence is not convincing.

So, for now, I continue to avoid demographics as a way to judge future inflation because the impact is so small that it doesn’t matter in practice. Instead, we need to look at other drivers of inflation that are magnitudes larger in their influence. Expecting inflation (or interest rates) to rise because of demographic shifts remains a fool’s errand in my view.

You make a strong case for what you are saying. I agree with Goodhart and Pradhan that we will have a nearly global labor shortage. That means an increase in the *relative* price of labor. With neutral monetary policy that would mean an acceleration of inflation, but with rock-star central bankers monetary policy is never neutral: they are always trying to accomplish some political goal or other, usually "full employment," but they may also be trying to keep rates low so governments can borrow more. So I agree that the Goodhart and Pradhan conclusion is not necessarily what is going to happen - it is more likely than not, but that's not saying much.

Ive been intrigued by their arguments and press noise. Demographics have a sort of compelling naturalness to them (such as the idea that the markets, broadly, will be driven lower by Boomer retirement asset decumulation). FYI There are some good podcast interviews as well. Thanks for your analysis here which is excellent as always