Japan is the playbook, not the exception

Last year, one part of my series against Cassandras focused on the fear of excessive government debt in the US and other countries. I explained why current debt levels will not lead to a debt catastrophe or a financial crisis anytime soon and I emphasised that Japan manages to sustain much, much higher debt levels for decades without problems. Furthermore, I showed how central banks can engage in financial repression to help governments sustain extremely high debt levels forever. A new study provides some wonderful analysis of how this works in practice in Japan.

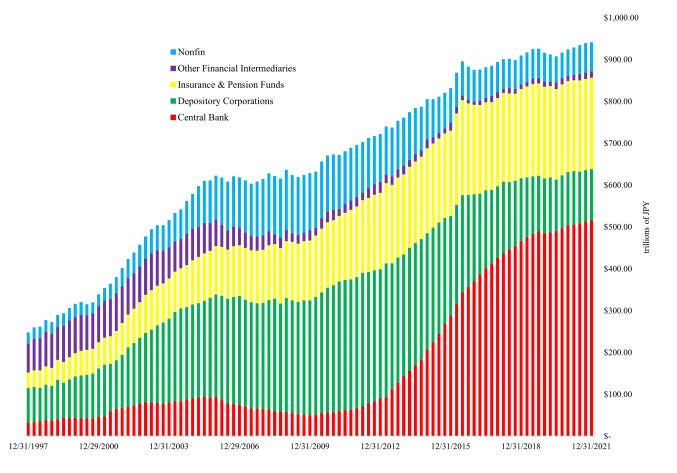

Let’s start with a look at who owns Japanese government bonds (excluding T-Bills and other money market instruments). Note the dramatic increase in the share of bonds owned by the Bank of Japan which launched its quantitative easing in 2001 but then turbocharged it after the financial crisis. Key to this massive increase in bond holdings by the central bank was the zero interest rate policy and the introduction of yield curve control, where the central bank stands ready to buy any government bonds as soon as yields drift above a certain threshold. In essence, the Bank of Japan guarantees the government that it will buy government debt at low yields, which is the same as saying it will buy government debt at (excessively?) high prices.

Japanese government bond holdings (excluding T-Bills)

Source: Chien et al. (2023)

Now, put yourself into the shoes of the Bank of Japan. The central bank’s balance sheet is invested in long-duration assets (i.e. Japanese government bonds) but its liabilities are defined by the reserves, commercial banks hold at the central bank and the currency in circulation. In other words, the central bank earns long-term interest rates and pays short-term interest rates or no interest at all on its liabilities. That is not different from what regular banks do by lending money to households and businesses with long duration but borrowing money in the form of deposits with short duration. Except that the central bank doesn’t really need to borrow money to finance its operations (remember, a central bank does not have double bookkeeping because it can print money at will to cover any losses or deficits, which is also why a central bank cannot go bankrupt).

While this kind of borrowing short to lend long is the essence of classic banking, the central bank can do this at levels that are much more extreme than what any commercial bank could do. Today, the Bank of Japan owns Japanese government bonds to the tune of 131% of Japanese GDP. Hence the government of Japan continues to borrow at low interest cost but with very long duration while the liabilities remain relatively short duration.

If one combines the government balance sheet with the Bank of Japan balance sheet, one can calculate the duration of assets and liabilities as well as the net duration of the government’s assets. As you can see from the chart, this net duration rose from 10 years in 2011 to 30 years today.

Duration of Japanese government (incl. Bank of Japan) balance sheet

Source: Chien et al. (2023)

In the study, the authors estimate that this kind of recycling of government debt via the central bank’s QE and yield curve control is likely to reduce government bond yields by about two percentage points and enables the Japanese government to not only sustain high debt levels indefinitely but to increase its borrowing capacity while servicing all existing liabilities. The financial repression by the Bank of Japan is so strong that it enables the Japanese government to pile on more and more debt without ever getting into trouble.

This has two important consequences.

First, the larger the duration mismatch between assets and liabilities becomes for the government, the stronger the incentive to keep interest rates low. You see, if the duration mismatch between assets and liabilities is large, then rising interest rates will lead to a massive financing problem for the government because its assets lose value much faster than its liabilities. However reducing interest rates leads to an outsized financing headroom for the government, so every government has a large incentive to influence the Bank of Japan to keep yield curve control in place and force long-term bond yields to very low levels forever.

Second, the artificially low yields on long-term government bonds mean that there is a redistribution of wealth towards owners of assets with long duration. These tend to be older and wealthier households who own homes and have larger investment portfolios. Younger and poorer households, on the other hand often must borrow at high interest rates with short maturities or have no investment portfolios and thus only earn short-term interest rates on their bank accounts. The result is that as financial repression continues to keep the government afloat, wealth is gradually shifted towards older and wealthier households which may lead to social tension in the long run.

I think it is crucial for investors today to understand these dynamics because as I keep emphasising, our future is Japan. In the US and Western Europe, the joint challenge of an ageing society and large debt levels forces us to follow in the footsteps of Japan. Expect the charts above to become the playbook for the US and Western Europe over the coming decades.

"Austerity" measures have a lot of fans who view national accounts as one big overgrown household budget, but against the backdrop you describe, the risk of triggering a "balance sheet recession" is very real https://en.wikipedia.org/wiki/Balance_sheet_recession

"Corporate investment, a key demand component of GDP, fell enormously (22% of GDP) between 1990 and its peak decline in 2003. Japanese firms overall became net savers after 1998, as opposed to borrowers. Koo argues that it was massive fiscal stimulus (borrowing and spending by the government) that offset this decline and enabled Japan to maintain its level of GDP. In his view, this avoided a U.S. type Great Depression, in which U.S. GDP fell by 46%. He argued that monetary policy (e.g., central banks lowering key interest rates) was ineffective because there was limited demand for funds while firms paid down their liabilities, even at near-zero interest rates. In a balance sheet recession, GDP declines by the amount of debt repayment and un-borrowed individual savings, leaving government stimulus spending as the primary remedy."

Hello Joachim, many thanks for this very interesting post!

I'd have a question.

Frankly I do not understand the correlation between the low-yield environment and a self-perpetuating wealth effect:

"Second, the artificially low yields on long-term government bonds mean that there is a redistribution of wealth towards owners of assets with long duration. These tend to be older and wealthier households who own homes and have larger investment portfolios. Younger and poorer households, on the other hand often must borrow at high interest rates with short maturities or have no investment portfolios and thus only earn short-term interest rates on their bank accounts."

Isn't it always the case, whatever the yield environment, that wealthy households get better borrowing conditions (longer maturities, lower interest rates) than poorer, hence for the borrower riskier households?