Is this the monetary policy of the future?

My series against Cassandras has inspired many interesting discussions with readers and I have already addressed two responses in posts before my summer hiatus. But one particularly interesting challenge came from reader JS. He took my argument that central banks have to follow in the footsteps of Japan because the high indebtedness of governments forces them to keep bond yields low to prevent a government debt bomb from exploding and asked a simple but powerful question: Assume you have a government with lots of debt and a central bank that uses QE to keep the cost of borrowing and bond yields low. Surely, they will have to abandon QE when there is an external inflation shock like we have seen in 2022?

Theoretically, that seems true. You would not want to fight inflation by hiking short-term interest rates while stimulating the economy by buying long-term bonds through QE measures. That’s like taking away with the left hand what the right hand gives.

But if you have a government that is extremely indebted, that may just be what a central bank has to do to prevent the system from collapsing.

Let me explain.

First, let us look at the central bank in the government with the highest indebtedness and its actions during the current inflation episode. In reaction to the inflation spike of 2022, the Bank of Japan did nothing.

National inflation rates arguably didn’t rise to the same heights as in the US or Europe, but by Japanese standards, the country experienced a pretty bad inflation push with annual inflation rates moving from -1% in mid-2021 to 4.1% at the end of 2022. Yet, the Bank of Japan did not hike interest rates. It didn’t even abandon its yield targeting policy where it fixes long-term bond yields. All it did was to allow bond yields to fluctuate in a wider band around the target and it even accelerated the pace of its bond-buying programme.

This is of course a different inflation scenario than the 10% inflation rates we saw in the US and much of Europe, so I would expect central banks in the West to hike interest rates in response to an external inflation shock just like they did in 2022. And they will do so even in an environment where government debt is very high.

But remember why central banks hike interest rates in the first place. They want to reduce demand in the private sector, not necessarily demand in the government sector.

This makes me wonder if central banks in a heavily indebted country could even go one step further. Could central banks reduce demand in the private sector by hiking short-term interest rates while protecting governments from rising interest payments by keeping long-term bond yields low? Would hiking interest rates at the short end while implementing QE at the long end of the yield curve work?1

Obviously, nobody knows for sure but here is my main argument why I think this could work. The duration of debt in the private sector is much shorter than it is for the governments. Thus, interest payments for mortgages, consumer loans, and business loans adjust much quicker than the interest payments the government has to make on its bonds. The result would be that the private sector will experience a slowdown of demand well before the government faces significantly higher interest expenses that could push the deficit into an ever-accelerating spiral.

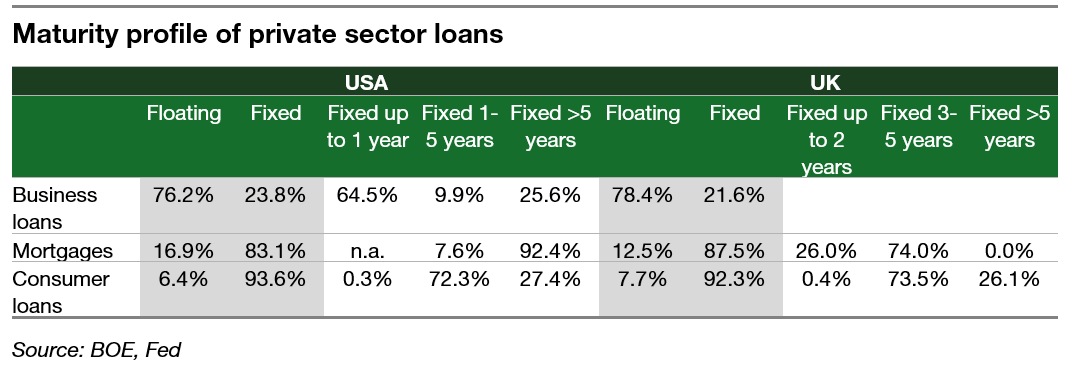

Let’s take a look at the situation in the UK and the US as an example.

It’s immediately clear that the average duration of consumer loans and business loans in the US and the UK must be less than 5 years because the vast majority of loans have a maturity below that. In the UK, where 5-year fixed mortgages are the norm even the average duration of a mortgage is below 5 years while in the US with its dominant 30-year mortgage the average duration is much higher.

But now let’s look at the average duration of government bonds issued by the UK and US governments. We exclude short-term financing vehicles with less than one-year maturity and end up with an average duration of government bonds in the US of 6.2 years and 9.1 years in the UK. In other words, it takes several years longer for the government to feel the pain of higher interest expenses than for the private sector.

It looks like it could be a viable monetary policy strategy to dramatically2 increase short-term interest rates while keeping long-term bond yield low through yield curve targeting. Then, you just sit there and wait. The pain will first be felt by businesses and private households which have to curb demand, triggering a recession and killing off inflation. Only with some delay will the government's cost of debt increase. If the central bank is aggressive in hiking short-term rates, it can effectively trigger a recession and put out inflationary fires before the government even feels material pain on the debt front.

Effectively, this would bail out a heavily indebted government while still allowing the central bank to target inflation and employment levels.

I invite readers to comment on this idea, but it seems to me this could be the get-out-of-jail card for heavily indebted governments…

Here it is worth mentioning that there is a common misunderstanding of the link between QE and inflation. If a central bank continues to buy bonds at unchanged speed this does not add fuel to the inflationary fire. What matters is the rate of change in the bond-buying programme. If the central bank increases the amount of bonds bought in the open market that is supposed to increase inflation while a reduction of bond purchases is supposed to reduce inflation.

The central bank would likely have to increase short-term rates more aggressively than normal because the long end of the yield curve is fixed by QE meaning that some of the pain from higher short-term rates will not be transmitted to the long end of the yield curve making harsher rate hikes on the short-end necessary to get the same impact on the real economy.

Very interesting and makes sense that this may work on the monetary policy side. But one element that would not be "held constant" is the impact of this monetary policy on tax receipts and government debt. Reduced economic activity will collapse tax receipts in the US at the same time that interest expense is outstripping tax receipts. This may be the achilles heel that causes the debt bomb spiral.

Your in-depth discussion of the nature and causes of inflation is always stimulating. In particular you are refreshingly frank in admitting that few know what is really going on, and those that do are keeping that knowledge to themselves. In such circumstances I usually fall back on the KISS principle as exemplified by the Latin phrase "Cui bono?" The fact stands that indebted governments have everything to gain from devaluing their currencies, and thereby their debt. The problem arises when inflation damages the economy. This is the mustang they are riding