How to spot a house price bubble

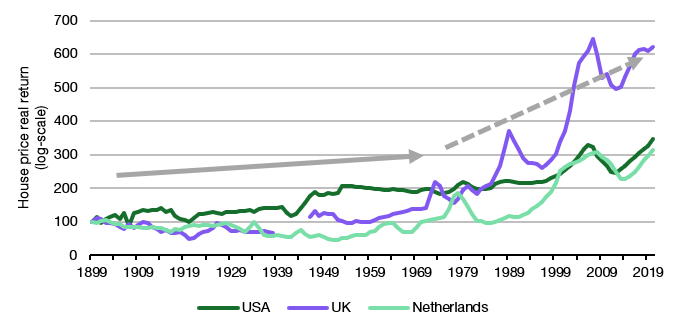

House prices have become so high that first-time homebuyers often find it hard to get on the property ladder. In particular since the 1970s, house prices, adjusted for inflation, have started to accelerate. This is visible as a steeper increase in real house prices in the chart below. But what drives this acceleration and how can we spot a real estate bubble in the making?

Martin Droes and Alex Van de Minne have examined Dutch house prices since 1900 to identify the main drivers of house prices in that country. Their results are informative on two levels.

House prices in the US, the UK and Netherlands since 1900

Source: Jorda et al. (2019), MacroHistory Lab

First, they show that until the 1970s, house prices were mostly determined by the cost of materials and labour to build a house, the supply of houses and population growth. But since the 1970s the drivers have shifted. Between 1970 and 2012 about 70% of the house price increase can be explained by the increase in capital and the cost of capital, while an additional 20% is explained by population growth. In other words, people have increasingly bought houses on debt (i.e. using mortgages) rather than buying them outright. And as mortgage rates dropped, people could afford to pay more for a house.

Today’s housing affordability crisis is simply a reflection of low interest rates, but it also implies that building more houses is unlikely to alleviate the problem for long. People will simply buy more houses and bid up the price of these houses again. It seems the only way to reduce house prices is to increase the cost of mortgages or reduce population growth even more than is already the case. But that is pure conjecture on my behalf…

In any case, their research points to a second important lesson for all investors. They find that if people do not allow for drivers of prices to change over time but instead assume a stable equilibrium in the long run, significantly overestimate the appearance of a house price bubble. What the research on house prices found was that over time the influence of different drivers changes relative to other drivers. If one examines house prices using a very long time frame, one implicitly fixes the impact of each factor to the average over many decades. The result is that the model becomes less predictive of what is going on in house prices and overestimates the possibility that house prices have deviated too much from fundamentals. Using models that allow for the influence of different drivers to change over time gives a more accurate result and prevents investors from identifying bubbles where there are none.

And I think this is a lesson that all investors need to heed. Just think of all the people who argue that the long-term average of equity market price-earnings ratios is 16x to 17x. Hence, markets trading at PE-ratios of 20x or more necessarily have to be in a bubble or at least overvalued. The flaw in this argument is the implicit assumption that the long-term average PE-ratio is still relevant in a time when capital markets, interest rates and inflation are markedly different than 50 or more years ago. And by sticking with such long-term models and its implicit assumptions of stable drivers of value, one can come to very different conclusions and for example avoid equity markets even though they are not in a bubble at all.

I have written about this ‘long-term effect’ for interest rates here and shown how your assessment if interest rates are low or high can change dramatically based on how far back in time you look. The research of Droes and Van de Minne shows that the people who see bubbles in financial markets implicitly assume that long-term relationships between drivers of markets and market valuations are constant over time. But remember, there is no law of gravity in finance and these relationships change all the time, making the identification of bubbles harder and more flawed than one thinks.

"No law of gravity in finance"? What do you think of this Buffett quote "interest rates are to asset prices, sort of like gravity is to the apple"

https://www.visualcapitalist.com/700-year-decline-of-interest-rates/

https://www.visualcapitalist.com/the-history-of-interest-rates-over-670-years/

I want to share with you these two graphs that show clearly what you mentioned about the long term outlook for interest rates. If you look at the first graph, you can notice that there is a kind of stationarity around a downward trend. This means that this time series always returns to the trend over time and any shocks or fluctuations are not permanent (assuming more rigorous statistical tests confirm this) unlike what would happen with a stochastic trend.

That said, I am very interested in the topic of how market drivers, market valuations and different actors in those same markets influence each other. I am conducting an in-depth research on this argument and I would like to share an extract of the introduction with you: "[...] The financial system, akin to DNA, is fundamentally a repository of information in the form of prices of the instruments that comprise it. This information serves as a catalyst for productive activity aimed at generating wealth.

Both systems (biological and financial) are characterized by randomness and necessity. In the realm of biology, randomness is exemplified by genetic mutations that encounter the necessity of environmental selection at the macro level. In the realm of finance, randomness is exemplified by economic and financial events that encounter the necessity of a system created by human agency with a pre-determined purpose. And both systems go through processes of continuous evolution and transformation. The evolution of the physical world, from the subatomic level to the most complex social phenomena, is characterized by cyclical patterns of growth and decay, creation and destruction. Similarly, the financial system is characterized by periods of expansion and contraction, boom and bust, and the continuous evolution and transformation of the system over time. These events can create opportunities for growth and development, but they can also lead to financial crises and economic recessions. In essence, the cyclic nature of these systems is a reflection of the continuous evolution and transformation of the sensible world itself, as it progresses through time.

The financial system is teleological in its individual components; the randomness that "impacts" the system is categorized, and the affected elements act accordingly. In this context, the information generated is constrained by the positions of individual actors, and as it emerges from their interactions, it remains strongly dependent on the initial settings (portfolio compositions) and the willingness (mechanical or conscious) of the parties to engage in transactions in the market itself; both of which determine the reaction to the randomness of financially significant events (that randomness is not just a matter of disorder versus order, but rather a reflection of a larger and more complex order that we have not fully understood or broken down into its essential components yet). [...]"