The arithmetic of high conviction portfolios

I recently wrote a post about the empirical observation that the bulk of the alpha generated by active managers is generated by their high conviction bets while their low conviction active bets tend to have a zero or even negative contribution to the portfolio’s active performance. The natural conclusion of that research is that active managers should run more concentrated portfolios focused only on their high conviction ideas. This was challenged by a reader with two interesting reports that argued that concentrated high conviction portfolios were not better due to a host of reasons. I encourage you to go to the comments section of the link above and read the posted notes and my responses.

But one challenge was really interesting. The reader pointed out the findings of the research by Hendrik Bessembinder some of which I have discussed here, here, and here. In essence, Bessembinder shows that the performance of the US equity market is highly concentrated in a few superstar performers, while the majority of stocks have poor performance and even underperform government bonds. This, Bessembinder argues, means that more diversified portfolios should have a better chance of good performance because they cast a wider net and thus have a higher likelihood of catching these superstar stocks.

I think this is too short-sighted, because while a more diversified portfolio has a higher likelihood of being invested in these superstar stocks, the performance contribution of these stocks to the overall portfolio is smaller. This is a result of the unfortunate reality that every portfolio has capital constraints. No portfolio manager can increase her investments infinitely, either because they are long only and thus can only invest the money they manage, or because they have lending constraints and can’t borrow infinite amounts of money to invest in stocks.

So, let’s have a look at how active portfolios perform in a market where stock performance is highly concentrated. To do this, imagine a stock market with 100 stocks. 99 of these stocks have a return of 0% and one stock has a return of 1000%. The average return of the stock market with all stocks weighted equally is 10%.

Now, let’s assume there are three different investors in the market:

The passive investor buys all 100 stocks in equal amounts and thus replicates the market.

The diversified active manager runs a portfolio of 50 stocks all equally weighted at 2% in the portfolio.

The concentrated high conviction active manager runs a portfolio of 20 stocks all equally weighted at 5% in the portfolio.

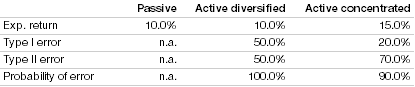

To get a feeling for the performance of these three investors let’s first assume that they are all unskilled and no better than chance at picking stocks. The table below shows the resulting expected return of the three portfolios (before fees and costs) and the type I and type II errors. The type I error is the probability of accepting a truly unskilled manager as skilled based on her outperformance. The type II error is to falsely classify a skilled manager as unskilled based on her underperformance. To get an idea of the size of error that can be made by investors I have (unscientifically) just added the probability of a type I and type II error (please no complaints, this is just a back of the envelope calculation).

Performance of unskilled managers with different investment approaches

Source: Liberum

As expected, the unskilled managers on average create no outperformance over the passive fund. But because the more diversified portfolio has more stocks in it, there is a 50% chance that some unskilled manager will accidentally stumble on the superstar stock and outperform the market due to the higher weight of the superstar stock in the active portfolio vs. the market. Meanwhile, in the concentrated portfolio, there is only a 20% chance that some unskilled manager will accidentally invest in the superstar stock and be identified as skilled, even though she isn’t.

Which brings us to lesson 1: In a concentrated portfolio, it is harder for unskilled managers to pass as skilled.

Now assume we have active managers who are skilled. But skill comes in different shapes. Let’s assume that the diversified active manager has 20 high conviction ideas, while the remaining 30 stocks in her portfolio are low conviction ideas. The concentrated active manager meanwhile also has 20 high conviction ideas but doesn’t invest in any stocks outside these. Now assume that the skill of the active fund manager comes in the form of a 50% better than chance likelihood of finding the superstar stock in the market and classifying it as a high conviction idea. Yet, the fund manager still continues to invest equal amounts of money in each of the stocks in the portfolio. The table below shows what happens then.

Performance of skilled managers with different investment approaches where skill comes as the ability to identify outperforming stocks

Source: Liberum

In this case, the skill of the active manager leads to outperformance vs. the passive fund. But because the weight given to each stock in the more diversified active fund is 2% while the weight given to each stock in the more concentrated fund is 5%, the expected outperformance of the concentrated portfolio is larger than for the more diversified portfolio. The probability of an unskilled manager to accidentally stumble on the superstar stock and outperform is unchanged to the first case above, but the probability of a type II error (i.e. an active manager underperforming and being classified as unskilled) is lower for the more diversified portfolio. The total likelihood of committing a type I or type II error is, however, the same in both cases.

Which brings us to lesson 2: More concentrated portfolios increase the career risk of skilled managers (i.e. being skilled but falsely classified as unskilled by asset owners).

Now, let’s go to the final iteration of our thought experiment. Assume that the active managers are skilled but not in identifying the superstar stock. Instead, they analyse each stock and based on that analysis, they put a higher weight in their portfolio on high conviction stocks. The more diversified active manager increases the weight of her 20 high conviction stocks from 2% to 3% in the portfolio and reduces the weight of the 30 low conviction stocks to 1.3%. This is not an option for the concentrated active manager because she only invests in her high conviction stocks anyway and thus invests 5% in each of these 20 high conviction stocks. The table below shows that that does to the expected return and the type I and type II errors.

Performance of skilled managers with different investment approaches where skill comes as the ability to increase the weight in high conviction stocks

Source: Liberum

Now, the outperformance of the skilled manager with the more diversified portfolio disappears while the outperformance of the skilled manager with the concentrated portfolio remains unchanged. The reason why the skilled manager with the more diversified portfolio suddenly no longer outperforms is that while the weight of the high conviction stocks increases the weight of the low conviction stocks declines. If the diversified active manager picks the superstar stock as one of his high conviction stocks, the outperformance will increase, but if she picks it as a low conviction idea, the outperformance will decline. Because there are 20 high conviction stocks in the portfolio and 30 low conviction stocks, the outperformance on average declines and in this case ends up disappearing altogether.

But the more important consequence of this phenomenon is that the probability of a type II error (falsely identifying a manager as unskilled even though she is skilled) increases. Thus, in this scenario, there is a high risk of falsely identifying an unskilled manager as skilled and a similarly high risk of falsely dismissing a skilled manager as unskilled. A diversified active portfolio becomes the worst of both worlds.

Which brings us to lesson 3: In a more diversified portfolio, a skilled manager has less room to create outperformance, which increases her career risk.

Looking at all these three cases in combination, we finally come to the final lesson for asset owners:

Lesson 4: In a more diversified active portfolio asset owners have a higher risk of falsely sticking with an unskilled manager while maintaining a significant risk of firing a skilled manager. Overall, the likelihood of making the wrong decision in selecting a fund is at least as high and sometimes higher for a diversified active portfolio as for a concentrated active portfolio.

Hi JK - You have raised some interesting points and I need to think about this some more. I will discuss with a business partner and get back to you. Hope all is well in London.

Regards,

Pete