The new divestment trend

For some time now, there has been a backlash against ESG investing. This backlash is arguably much more pronounced in the US where the topic has become politicised than in Europe. Plus there are cultural differences that can explain attitudes toward ESG investing. However, how big is this backlash really? I mean in numbers rather than airtime and noise?

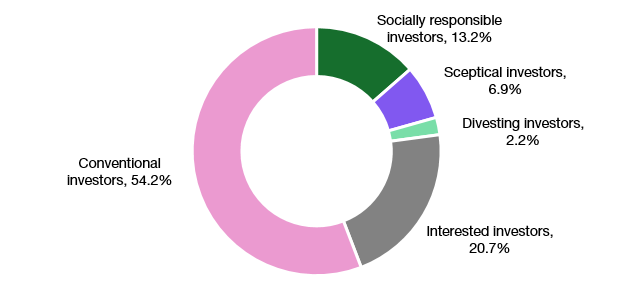

A team from the University of Kassel in Germany asked 1,095 German private investors about their attitude towards ESG investing and, crucially, asked them not just whether they currently did or intended to invest in ESG funds, but also whether they wanted to divest. This allowed them to group the respondents into several categories:

By far the largest group were the conventional investors who did not own sustainable investments and did not plan to do so in the next three years. They make up more than half the surveyed group.

On the opposite end of the spectrum were the socially responsible investors who currently own sustainable investments and intend to continue to invest in them. These accounted for 13.2% of the surveyed households.

Then there were the interested investors, which form the second largest group at 20.7%. these investors currently do not own socially responsible investments but plan to invest in them in the next three years.

Among the potential or actual divestors are the sceptical investors who currently own socially responsible investments but intend not to increase their allocation (but also not decrease it).

And finally, there are the ESG divestors who currently own socially responsible investments but have become so disillusioned that they intend to sell them in the next three years. These make up 2.2% of the respondents.

Investor groups in Germany

Source: Eckert et al. (2024)

First note the relatively small share of investors who actively divest from sustainable investments. 2.2% of the total sample or about 10% of all investors who currently own socially responsible investments.

As I mentioned above, the backlash against ESG tends to be stronger in the US than in Germany or Europe in general, so I guess the numbers are a lower bound for the disillusioned investor group, but still, I find them rather low in any case. These critics of ESG investing certainly occupy much more space in the public discourse than seems warranted by these results. But then again, I guess most critics aren’t even in this group. Rather, they have never invested in sustainable investments and never will and thus are a subgroup of the conventional investors.

In any case, the share of respondents that are not currently invested in sustainable investments but plan to do so is almost ten times the size of the active divestors. Why do they want to invest sustainably and why do the divestors want to get rid of their investments?

The survey gives some preliminary answers but there is certainly more to do. But in general, one of the key findings was that the social environment (family, friends) of an investor has an outsized influence. People who invest sustainably do so because their social group is doing it and they feel some kind of peer pressure. Conventional investors, meanwhile, remain conventional investors because they feel less peer pressure from family and friends to invest responsibly. In short, your social network has a much more important influence on your investment decision than most people would admit. If you mix and mingle with people who are enthusiastic about ESG you are likely to become enthusiastic about it as well. If you mix and mingle with people who think this is all nonsense, you are likely to think that as well. Neither group exerts independent decision-making skills (though some like to pretend they do). Both groups are just following their herd.

A second driver was the perceived attractiveness of sustainable investments in terms of returns. This was the main driver behind divestors’ intentions to sell their sustainable investments. They simply feel the returns haven’t lived up to their expectations or that much of their investment engage in greenwashing. In that respect, they are like conventional investors who also don’t think sustainable investments are more attractive than conventional investments.

Notably, though, the attitude of divestors toward sustainable investments does not reflect an attitude toward sustainable consumption more generally. Divestors are less likely than the average person to ignore sustainability issues in their consumption choices when buying stuff. They just don’t think that sustainable investments make a difference.

I ran a global sustainability fund for a European fund manager for a few years, and perhaps my pragmatic American side came out when I'd pitch why I thought applying ESG criteria in holistic investment analysis was useful: "it generally helps you identify bad management behavior, and if you avoid that, you avoid torpedoes in your portfolio".

That said, one of the most important reasons our fund posted better-than-benchmark results was that we had 20% leeway in our fund guidelines to buy stocks which might not *yet* meet all the ESG criteria, but were on the way to doing so. Our competitors were generally restricted to only buying stocks that an external ratings agency had *already* selected and rated as ESG-compliant, so their customers were essentially offered a high-fee index fund with the stock picking done by desk analysts at a third-party data provider. I used to joke "that's a bit like having a fund restriction requiring the PM to only buy stocks witha P/E within one standard deviation of the market P/E, with no opportunity to bottom-fish value stocks nor buy high-P/E stocks that grow into their valuations over time".

Plus, over time we discovered some of the criteria were capricious: One data vendor took great pains to deliniate the makers of light chocolate and dark chocolate, but then black-listed any firm that made "turbines"; they were screening out makers of jet warplanes, but that also meant no wind turbine manufacturers made the cut. One morning we woke up and discovered that one megacap US tech company was blacklisted because the agency had unilaterally determined that "it didn't abide by the spirit of European GDPR". Okay, but one could say that about *all* megacap tech companies, so why that company in particular? And what about the "truthiness" aspect of spirit vs. letter of the law? There was also evident geographic bias in negative scoring; Nike and Adidas used practically identical supply chains and subcontractors, and have very similar enviromental footprints (no pun intended), but you can guess which always seemed to receive higher scrutiny.

robeco does passive ESG for resilience.

wellington and pzena does more ESG inflecting companies, sometimes as suggestivists.

i presume their data well informs them whether this effort provides risk-adjusted alpha.

its not a coincidence that all offer low-cost vehicles, but is it because they themselves want some ESG or due to competition? or simply because regardless, it works.