The Virtuous Investor: Rule 16

Never give up – The world may look bleak at times, but you can recover

This post is part of a series on The Virtuous Investor. For an overview of the series and links to the other parts, click here.

“I have perceived to happen unto many, whose minds are naturally somewhat feeble and soft without resistance, that after they were once overthrown, they ceased to wrestle anymore.”

Erasmus of Rotterdam

Here is a one-item IQ test for you:

Would you rather get promoted or lose your job?

I guess most people prefer to get promoted and that is understandable. What happens in our mind when we ponder the two options is, we simulate our life either after the promotion or after being let go. And obviously, we imagine our life to be much better after the promotion. We have a higher salary, more influence to achieve the goals we think are important, a bigger car, a prettier girlfriend, etc.

And that is all fine and well, but simulations have one big disadvantage: They typically ignore the short-term struggles that are needed to get to the goal. While a promotion might be a great thing, it typically comes with more work and longer hours and in our mental simulation of the two outcomes, these longer hours, the difficult discussions with direct reports and the office politics don’t feature at all. Simulations are abstractions and sometimes, these abstractions miss some crucial details.

Just imagine you would be going on a vacation into the Caribbean. The images that form in your head are you sitting on a beach with a nice drink, doing nothing and enjoying the sun. What you didn’t imagine was the hassle of getting through airport security, trying to catch some sleep while the guy next to you is snoring loudly or the possibility that it might rain constantly at your destination.

If people are asked how happy they think a promotion or a vacation will make them, they consistently think they are going to be happier than they really are once they get the promotion or go on vacation.

As investors, we face the same problem. If I am presented with a portfolio designed to fit my risk preferences and structured to give me the best chance of achieving my retirement goals, then I will usually look at the simulated development of my retirement wealth as shown in the chart below.

Expected development of retirement savings

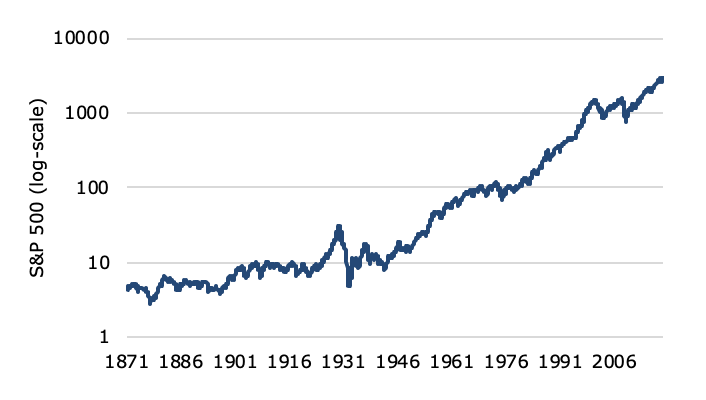

But in reality, the ride isn’t that smooth. Take a look at the S&P 500 since 1871 below. Looks great, doesn’t it? Yes, there are some setbacks but in the long run, I will be fine.

The S&P 500 since 1871

Source: R. Shiller website.

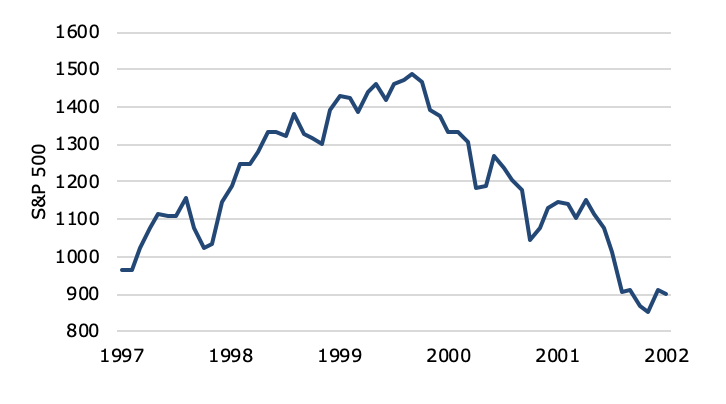

Well, here is my personal experience with the stock market after the first five years of becoming a professional investor.

My first five years as an investor

Source: R. Shiller website.

Five years is a long time and after these initial experiences, I was ready to throw in the towel on stocks and on tech stocks in particular. What I didn’t do when I started my career was visualise and simulate the ups and downs of the stock market as I worked towards my long-term goals. And when these ups and downs materialised, I was tempted to give up. This is when I learned not to look at my portfolio too often as I have described in rule 11 and compare my actual performance to the expected range of outcomes as I have explained in rule 6. But I still wasn’t prepared for how long I could remain under water with my investments.

I wish, a more experienced investor or an adviser would have taken me to the side and told me that no matter how much I think I understand volatility, nothing I simulate in my head will match the true viciousness of living through a bear market. The always great Jason Zweig recently wrote a great reminder of this challenge in his weekly Wall Street Journal column. Looking back at the crash of 1929, he concludes:

“To be a long-term investor in stocks, you have to be prepared to lose more money for longer than seems possible. Anyone who takes that risk lightly is likely to sell out, in the next crash, near the bottom.”

Yet, one of the reactions to this column was this:

In my view not preparing your clients for the possibility of massive losses and a long time under water is a dereliction of duty. And if you don’t prepare yourself for the possibility of being under water for much longer than you expect, you are not doing yourself a favour as an investor.

The charts below show the longest time under water going back to 1970 for several asset classes so you can prepare yourself for the bitterness of the fight.

Maximum time under water for different asset classes

Source: Datastream, Bloomberg. Note: All data in US Dollars and total return.

Maximum time under water for different asset classes including gold

Source: Datastream, Bloomberg. Note: All data in US Dollars and total return.

In the end, my portfolio will be alright – even if I invest in gold, but in the midst of a drawdown, I need to go back to these charts and compare my current experience to the worst-case situation shown in them. And every time I do that, I have to remind myself that even in the worst-case scenario, if I didn’t abandon the investments and gave in to the temptation of abandoning all hope, I would have come out alright in the end. Or as I said in rule 10:

This, too, shall pass away.