What if it doesn’t?

Today is the last ‘serious’ post of the year. Tomorrow, I will publish my usual cheeky Friday post and on Monday, you will receive my annual Christmas edition.

As most of us in the West will take some time off at the end of the year, I want to invite you to think about your investments and what the next year and the years thereafter will bring. In particular, I want you to consider all the ways in which you could be wrong.

Over the last several weeks and into early January, I am going through this process professionally, as I write my big annual outlook for 2022. And one of the topics that I wrestle with is the topic of inflation. I am still in the camp of the people who believe that current inflation (in particular energy price inflation) will be transitory and decline once demand for energy drops after winter. I am not as sanguine about inflation as the Federal Reserve is in that I expect inflation to be higher than what the Federal Reserve predicts, but I still think inflation will decline next year and the years after.

But what if it doesn’t?

What if energy shortages and supply chain disruptions persist throughout 2022? What if higher energy prices come through in the form of higher real wages and we get a wage-price-spiral similar to the 1970s? How would that affect my portfolio and how would I change my investments if this were to happen?

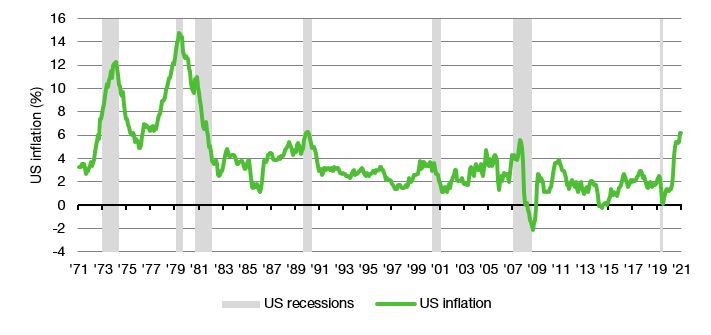

US inflation over the last 50 years

Source: Bloomberg

And then, once I have done that, I do something else, namely think about why the scenario I think will not happen, should not happen. This is where it gets difficult because our natural impulse is to just dismiss developments that contradict our pre-conceived notions without much examination. Our natural instinct is to engage in hand waving and assume that things have always reverted to some normal after a while. In a sense, I argue that inflation will revert to some pre-pandemic normal, while people who think inflation will get out of control argue that it will revert to some normal we last saw in the 1970s and 1980s.

But remember that there is no law of gravity in finance and over the last three years of writing this blog, a constant theme throughout has been how the world has changed substantially since the financial crisis and no longer works in the same way it did in the 1980s or 1990s, let alone the 1970s.

So, I have to force myself to explain how things will work out and use data, not anecdotes. And I challenge you to do the same with your opinions and expectations. If you argue with anecdotes or other rhetorical pitfalls like slippery slope arguments (i.e. the classic ‘if we allow this to happen and don’t fight inflation now, it will entrench itself and get out of control’) you have lost all credibility in my eyes and I will file your opinions in the drawer labelled ‘ideologue’.

The golden rule is to only dismiss an outcome if you can show beyond a reasonable doubt that it cannot happen and why it cannot happen. If you can’t do that, consider the option that you will be wrong and what that means for your investments.

By now, many of my readers will be smiling because my view that inflation will be transitory is the one view where I get the most pushback from investors these days. Contrary to economists, it seems as if it has become consensus amongst professional investors that inflation will get out of hand next year.

But here is one topic for these people to ponder. Along with the conviction that inflation (and interest rates) will have to reverse a decades-long trend and start to rise comes a conviction that stock markets are significantly overvalued. The number of charts that show how the US stock market is overvalued goes into the hundreds and one of the most common ones is the cyclically-adjusted PE-ratio popularised by Robert Shiller. So many investors have argued for more than a decade now that current valuations are unsustainable and have to come down. And they have been wrong for more than a decade.

So my question about US valuations coming down is: What if it doesn’t?

US cyclically-adjusted PE-ratio (CAPE)

Source: R. Shiller database

I don’t think I have ever responded to. a newsletter two days in a row, so this is a first and the result of your having written two excellent pieces on consequitive days.

Tendentially I find myself just on the other side of the “transitory” or “endemic” inflation line to you. But mine is a strong opinion weakly held. I see the same underlying and powerful deflationary pressures that you presumably do, see the supply chain bottlenecks as more or less a temporary phenomenon (I have four containers of product that have been waiting for over three months to be processed through LA Port so ‘supply chain disruptions’ is not a theoretical for me) and am sanguine about a resurgent boom: the shock to confidence and the exposure of incalculable ahut downs is having a severe effect on long term CAPEX. However inflation is the onlybway out of the hole governments have dug for themselves and they will continue tonabuse their “exorbitant privilege” until the printing press breaks. When that happens is anyone’s guess but the range of probable and potential outcomes is large that the caution around taking dogmatic positions is well made. Great post (even better than yesterday’s)

Joachim, I am a big fan of your newsletter/ blog/ substack/web3 project, especially the fact you keep us updated on academic research. Since you post daily but I can't read the posts daily I would love to have a weekly roundup of things you wrote, perhaps publish it on Thursdays. Perhaps something for you to think about doing in 2022.

I especially loved your piece on central bank digital currencies, thank you very much for writing that. To be honest I am sure I missed a lot of posts so I wonder what were your personal favorite (s) to write or the one(s) that got the most reactions?

Another suggestion for your end-of-year piece, if possible include some things about the "Starting position of the different markets and "things I bet won't change".

Again I imagine that writing this blog takes a lot more time than we think it does so a big thank you.