The Virtuous Investor: Rule 17

Always have a plan – It is your most effective weapon

This post is part of a series on The Virtuous Investor. For an overview of the series and links to the other parts, click here.

“Nevertheless the only and chief remedy which of all remedies is of most efficacy and strength against all kinds either of adversity or else temptation is the cross of Christ.”

Erasmus of Rotterdam

In my discussion of the first rule of the virtuous investor, I have pointed out how valuable a financial plan can be. There, I showed the results from a study by Annamaria Lusardi and Olivia Mitchell that people who followed even a simple planning rule were materially better off in retirement than people who did not follow a plan.

Since then, researchers have started to focus some more on the benefits of financial planning. For me as an investment specialist, the simplest way to think about the benefits of financial planning is in terms of the gamma concept introduced by David Blanchett and Paul Kaplan.

Gamma is pretty easy to understand.

In the investment world, we constantly talk about alpha and beta, where beta is the systematic risk of a portfolio and alpha is the outperformance created by an investment manager over a benchmark (adjusted for beta). Alpha is the most elusive animal in the entire investment world, constantly appearing in unexpected places just to disappear once you have put your money where it last showed up. Yet, many investors and advisers continue to be obsessed about hunting for alpha and while there is no guarantee, the recently published book The Return of the Active Manager by C. Thomas Howard and Jason Voss is in my view one of the best guides how to find alpha as an investor. You may want to also check out Jason’s blog, which is highly recommendable, should you not be subscribed already.

But besides alpha, there is also the additional return you can gain by making smart financial planning decisions. This additional return is called gamma by Blanchett and Kaplan. There are several possible sources of gamma:

The additional return gained by looking at your total wealth instead of just your investment portfolio. We all have many assets outside of our investment portfolio reaching from our house to life insurance and annuities, as well as our biggest asset, our ability to earn money through gainful employment (aka human capital). Taking these nonbankable assets into account often allows investors to take on much more risks in their portfolios than they otherwise would have, which in turn leads to higher wealth accumulation in the long run.

Most retirees still work with constant withdrawal rates, assuming that they can withdraw for example 4% of their portfolio each year (adjusted for inflation) to help finance their retirement. But markets don’t deliver a constant return. Sometimes returns are better, sometimes they are worse. And if you are able to dynamically change your withdrawals (taking out more after a series of good years and less after a series of bad years) this will, in the long run, enhance your retirement income. Such dynamic retirement withdrawal strategies are not easy to implement for private investors, which is why they should seek the help of a qualified financial planner if they want to do that.

Of course, if your retirement withdrawals aren’t the same every year anymore, you need some income to fall back on in hard times. Annuities are the right tool to help you do that. But what am I saying: annuities can be a valuable tool for almost any investor, as long as you are advised properly and don’t pay too much in fees for inadequate products, something that abounds in the annuity market, unfortunately. Nevertheless, allocating some of your retirement savings to an annuity that pays income no matter how long you live is an important planning tool that can generate gamma.

Asset location decisions can also generate gamma. By allocating some of your assets in tax-deferred or tax-exempt accounts where earned income can accrue undisturbed over time can be a great source to build additional wealth. And withdrawal strategies can enhance the gamma generated from these tax-advantaged accounts if the withdrawal strategy tales money from taxable accounts first and lets tax-advantaged assets grow as long as possible.

Asset-liability investing is the final tool to generate gamma. Commonplace for pension funds and other institutional investors, private investors rarely, if ever, think about their liabilities (ranging from personal inflation rates to currency risks). If you can invest your assets in such a way as to minimize the risks relative to your liabilities then you can gain a lot of additional lifetime income.

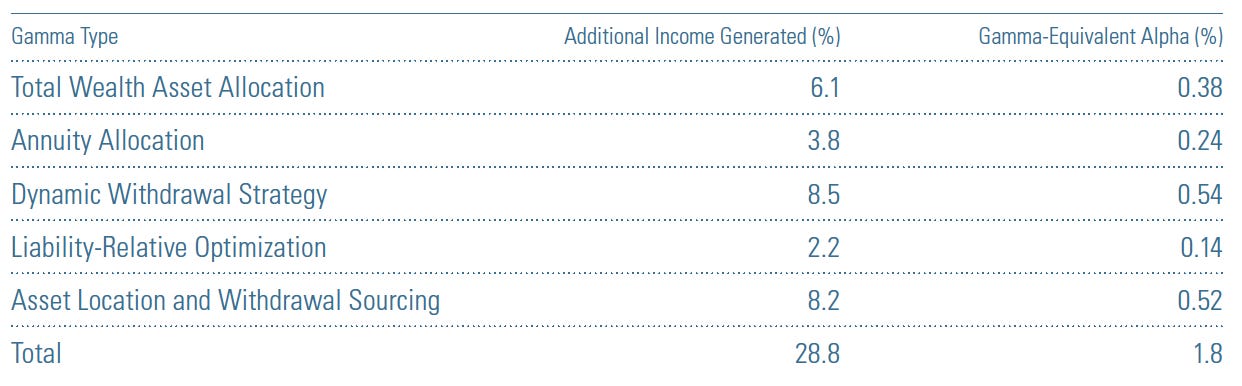

Blanchett and Kaplan have simulated the additional lifetime income generated through these strategies as well as the equivalent alpha an investor would need to generate on her portfolio to get the same result. The chart below shows that starting with a simple portfolio of 20% equities and 80% fixed income that is managed with a 4% annual withdrawal rate the gamma that can be generated by these different approaches is about 29% or 1.8% per year. I dare anyone of my readers to find that kind of alpha in their investment portfolios. It is quite a tall order. As the breakdown in the chart below shows, the biggest contribution to gamma was made by asset allocation decisions and by engaging in dynamic withdrawal strategies, while asset-liability optimization made the smallest contribution.

Estimated gamma from different financial planning strategies

Source: Blanchett and Kaplan (2014).

Which brings me to the question of how to learn about these techniques and find an adviser who can help you implement these planning strategies. In a recent follow-up study, David Blanchett looked at the answers to the US Survey of Consumer Finance between 2001 and 2016. The main result is shown in the chart below. It shows that only a minority of investors have a financial planner. The majority relies on the internet for financial advice, which is increasingly replacing friends as a key source of financial advice. Thank goodness for that.

Sources of investment and savings information for US households aged 25 to 55

Source: Kaplan (2019).

What worries me though, is that about the same share of investors use transactional advisers (i.e. brokers) instead of financial planners. But brokers have no fiduciary duty and only have to follow the suitability standard. As a result, they may not have the clients’ best interest at heart. And the study looks at exactly that difference. What is the influence of brokers on an investor’s investments compared to planners?

As it turns out, the average impact of financial planners on gamma and retirement wealth is positive, while the average impact of brokers is negative. Clients who have a financial planner are significantly more likely to have adequate emergency funding. In fact, if you have a broker as an adviser then you are less likely to have emergency funding available than if you have no adviser at all. Similarly, clients who are advised by a financial planner are more likely to have life insurance and annuity products that provide stable income than clients who are advised by a broker. And both of these safety nets taken together mean that clients of financial planners can have portfolios with a higher risk in place that in the long run provide higher returns.

Of course, that does not mean that you cannot get good advice from a broker or you are sure to get good advice from a planner, but your odds of getting good advice from a broker are certainly much lower than in the case of a planner. What is more, Blanchett also had something to say about the hypothesis that brokers are often investment specialists and thus may provide great advice in one area but not in others. I let David Blanchett have the last word:

“It’s not that households working with a transactional adviser were doing one thing really well and everything else poorly; they were doing everything poorly.”